August 2023 update: Labor markets continued their gradual normalization in July

Head of Economics and Global Labor Markets at LinkedIn

Subscribe to these updates here.

Global: Despite persistent challenges, the economy demonstrates near-term resilience

Global: Despite persistent challenges, the economy demonstrates near-term resilience

The cumulative increase in central bank policy rates to combat inflation is still pressuring economic activity. The global headline inflation is predicted to experience a gradual decrease over the next 12 months. On the other hand, underlying (core) inflation is expected to decline at a slower pace during the same period.

Despite the central bank tightening, economic activity in the second quarter of 2023 has proven resilient, in part supported by robust, albeit cooling, labor markets (particularly in the service sector).

The pace of hiring declines is gradually slowing down

Hiring rates are continuing their year-over-year decline, albeit at a slower pace across various countries. Notably, Singapore, Sweden, and Canada, alongside India, the U.S., the UK, Brazil, France, the Netherlands, Australia, and the UAE, have witnessed a deceleration in year-over-year hiring. Conversely, Ireland, Italy, and Germany have experienced an increase in year-over-year hiring compared to the previous month.

Labor markets continue to cool, but only at a gradual pace

Employers are gradually reasserting their bargaining power in the labor market as evidenced by the declines in labor market tightness observed in various countries, with LinkedIn's measure of labor market tightness approaching pre-pandemic levels. Notably, the U.S., United Kingdom, Canada, India, Ireland, and France are experiencing increased slack in their labor markets.

On the other hand, certain European nations such as Germany, Italy, and the Netherlands still contend with relatively tighter labor market conditions compared to their pre-pandemic baseline.

This cooling trend indicates a potential shift in the balance of power, favoring employers and suggesting a reduced influence for workers in the job market. Consequently, this development is expected to contribute to a slowdown in wage pressures, as employers have a relatively larger pool of applicants to choose from.

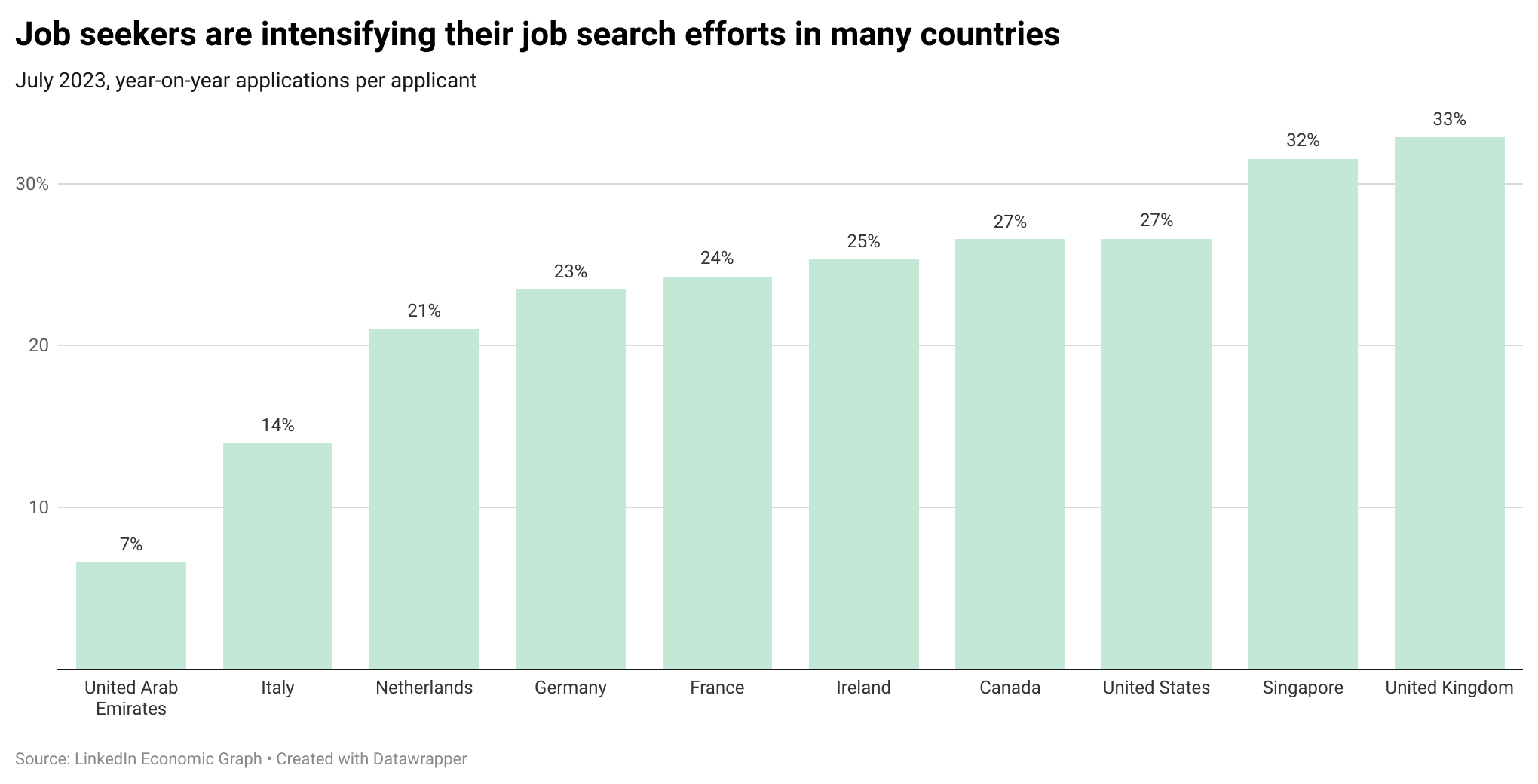

Job seekers are searching more frequently, realizing that they may no longer have the luxury of time

The current uncertainty in the outlook has driven a surge in job seekers intensity of search across various countries. In the U.S. and Canada, there has been a 27% year-on-year rise in LinkedIn applications per applicant. The United Kingdom, and Ireland also saw significant jumps at 33%, and 25%, respectively. The more modest increases in the UAE observed a lower 7% increase, likely due to the influence of the summer and vacation season.

A possible driver of the uptick in job seeking intensity might be found in a recent shift in members’ stance. Recent trends in the US LinkedIn feed have shown mentions of "open to work" have increased 3% in July while members' posting referencing a recession increased 12.6%.

U.S.: The recession narrative is evolving into a soft-landing narrative

The recent GDP report on economic growth provided highly encouraging results. The second-quarter economic growth, annualized at 2.4%, significantly surpassed the initial projections of a 1.8% gain. Moreover, this marks the fourth consecutive quarter of growth at 2% or higher, indicating a sustained positive trend. Another positive aspect was the composition of growth, which displayed promising figures. Notably, consumer spending and fixed investment both saw solid gains, while inventory accumulation remained at a mild level. These positive indicators suggest a favorable economic outlook and highlight the strength of the current growth trajectory.

Moving ahead, GDP growth is anticipated to slow due to diminishing job gains, which can be attributed to a scarcity of available workers and cautious corporate decisions to reduce capital spending. Nonetheless, there are several positive factors mitigating the potential drag on the U.S. economy in 2023. The housing market shows signs of stabilization, even with elevated mortgage rates, as persistent supply shortages maintain high prices and encourage new home construction. While global growth is not experiencing a booming phase, it is deemed sufficient to support moderate growth in exports. Additionally, hiring by state and local governments is partially offsetting the impact of federal fiscal policies.

Furthermore, regional banks have shown increased stability after a mini-crisis in March and April. Despite facing challenges like an exceptionally hot summer and international tensions, the economy has thus far managed to avoid the environmental or geo-political events that have historically triggered recessions. Moreover, US financial conditions have eased substantially, returning to approximately the levels observed in the spring of 2022, as indicated by the Financial Conditions Index of the Federal Reserve Bank of Chicago.

Amid these developments and with the labor market remaining resilient, there is a sense of cautious optimism surrounding the economy, suggesting a potential "soft landing" rather than the feared full-fledged recession.

Jobs data shows a steadily normalizing labor market

Employment continues to exhibit robust growth, and unemployment remains at low levels. The stock of U.S. paid job openings on LinkedIn reached its peak in March of the previous year, surging by 80% year-over-year compared to the prior year. Subsequently, the excess demand for labor has shown signs of easing, with job openings gradually decreasing, although they still remain significantly higher than the pre-pandemic levels.

People are returning to the office

Employers’ push to return to the office in person continues. Since the start of the year the share of paid hybrid jobs has exceeded the share of paid remote jobs, with the share of hybrid roles now at about 13% and remote at 9%. Furthermore, combined with a notable resurgence of job seekers returning to the labor market and engaging in more active job applications, the labor market is more competitive for the overall pool of applicants.

Collectively, the data indicates a gradual rebalancing of the labor market, facilitating a moderation in wage growth and a slow cooling of inflation. As of August 1, 2023, LinkedIn’s labor market tightness ratio stands at 1 open job for every 2 active applicants on LinkedIn, which indicates that the labor market remains relatively tight, even though it has cooled down from the high levels of 1 open job per applicant that we observed last year.

As we progress into August 2023, companies continue to offer fewer remote work opportunities while favoring hybrid work arrangements. The number of applications to remote jobs has begun to dwindle, whereas applications to hybrid positions continue to grow.

In July 2023, approximately 9% (1 in 11) of U.S. paid job postings on LinkedIn were offering remote work, while 13% were for hybrid work. This marks a notable decline in remote job offerings from the preceding year when they accounted for 18% of U.S. paid jobs. In contrast, the percentage of hybrid jobs has steadily risen since July 2022, increasing from 8% to the current figure.

Interestingly, despite the decline in remote job postings over the past year, paid remote jobs continue to attract an outsized share of applications (44%) and views (39%). Similarly, paid hybrid jobs, with 19.8% views and 19.8% applications, also garner significant attention from job seekers. Overall, 2/3 of job applicants applied to at least one remote or hybrid role last month.

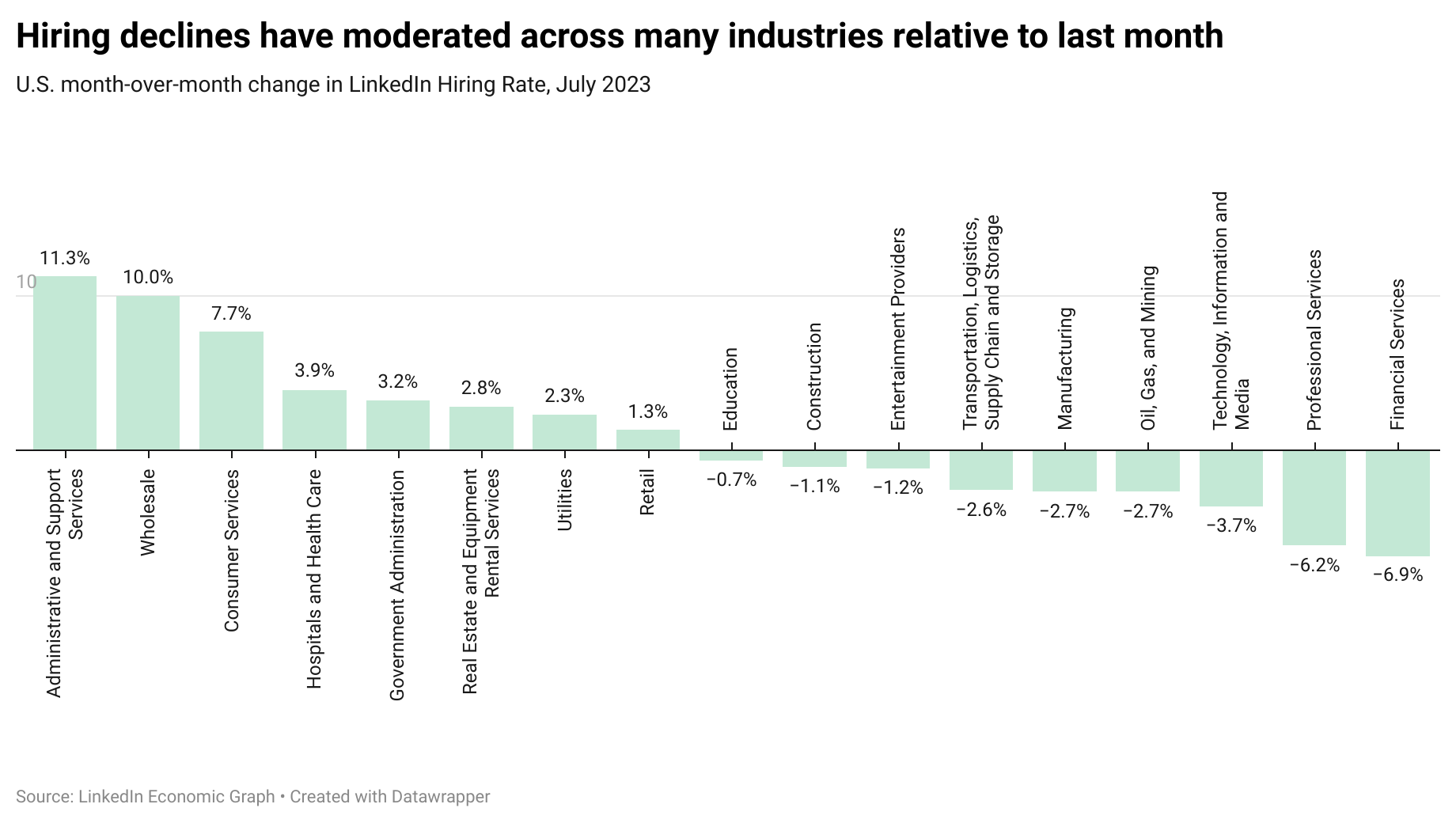

The month-over-month pace of hiring declines has eased in various industries compared to the previous year

In comparison to the prior month, hiring witnessed an overall increase in 9 out of 20 industries. Among them, Administrative and Support Services, which includes Staffing and Recruiting firms, experienced the strongest month-over-month gain (+11.3% m-o-m). However, it's important to note that despite this gain, hiring in this industry remains significantly lower (-25.2%) than in July 2022. Other notable sectors with positive growth include Wholesale (+10.0% m-o-m), Consumer Services (+7.7% m-o-m), and Hospitals and Health Care (+3.9% m-o-m).

On the other hand, Professional and Financial Services faced some of the largest drops in hiring compared to June 2023 (-6.2% m-o-m and -6.9% m-o-m respectively). Technology, Information, and Media experienced a more modest decline of 3.7% compared to June but continue to struggle significantly, being down nearly 40% compared to July 2022, making it the industry with the most significant decline.

Real Estate hiring also remains depressed compared to July 2022 (-15.8%), but it has shown a better performance this year with only a slight decrease of -0.7% since January and a growth of 2.8% compared to June, as a sign of stabilization in the housing market.

Eurozone: Tight labor market conditions persist in Europe

Several cyclical and structural headwinds have been a drag on the Eurozone area recently and are tilting near-term risks to the outlook to the downside. There're also offsetting tailwinds, but their mostly structural nature means their impact will be more gradual.

The primary factor causing a slowdown is the synchronized tightening of monetary policies worldwide. The delayed impact is due to the lagged effect of monetary policy. This drag is further intensified by the post-pandemic shift in global consumer preferences, which is moving away from goods and back towards services.

In general, the eurozone economy’s outlook appears fragile, particularly in the near term. This is due to various factors, such as demand being impacted by an unfavorable inventory cycle, anemic manufacturing, a structural decline in competitiveness in certain key sectors, and the presence of global policy headwinds.

Several European countries, including Germany, the Netherlands, Spain, France, Sweden, and Ireland, are experiencing significant year-on-year declines in hiring, ranging from 17% to 28%. These declines are attributed to economic uncertainty and labor shortages across various industries. Despite this trend, employment opportunities remain available, with the ratio of job openings to active applicants still higher than pre-pandemic levels in most countries. Additionally, unemployment rates across Europe are historically low or close to them, indicating a relatively robust labor market. This resilience can be attributed to variations in downturns across different sectors and their timings.

United Kingdom: Outlook is clouded by prolonged higher interest rates

The growth trajectory of the United Kingdom is anticipated to experience fluctuations over the coming years. It is projected to decrease in 2023, before making a recovery and rising to around 1.0 percent in 2024. The stronger-than-expected consumption and investment, driven primarily by the confidence boost arising from falling energy prices, justified a positive revision for 2023. Additionally, the financial sector has demonstrated resilience, aiding in the recovery, especially as the March global banking stress subsides.

The UK labor market has experienced a rise in slack and a continuous decline in hiring since the previous summer, indicating reduced demand for workers. Recent data from July 2023 shows a substantial year-on-year decrease in hiring activity, with a significant decline of 20.3%.

Asia Pacific: APAC’s labor markets remain resilient amidst weakening exports and inflation challenges

In Asia, domestic demand remains resilient amidst monetary tightening, while external demand for technology products and exports shows a decline. Headline inflation exceeds central bank targets in most economies, even as it recedes. Core inflation gains significance as a driving force for headline inflation and shows persistence.

Australia's labor market stays relatively tight with four applicants per job opening, reflecting a slowdown from the peak in 2022 but above pre-pandemic levels. Singapore also exhibits comparable tightness, with nearly five applicants per job opening, but experiences a significant 28.3% year-over-year decrease in the LinkedIn Hiring Rate, indicating a slowdown in hiring activity. India's labor market cools further, with around 20 applicants per job opening, and year-over-year hiring on LinkedIn declines by 23%, indicating tightening labor market conditions.

LatAm: Brazil’s economy grapples with high interest rates and policy uncertainty, while Mexico's growth weakens amid inflationary pressures

Brazil's economy is gradually slowing due to high interest rates, reduced external demand, and policy uncertainty. Labor market tightness in Brazil is decelerating, with hiring down by nearly 20% year-over-year in July, and nearly 43 applicants per job, indicating labor market slack.

On the other hand, Mexico's labor market is experiencing a gradual transition with nearly 12 applicants per job opening. The country's economic prospects are tied to the U.S., and as the U.S. economy slows down, Mexican exports and remittance inflows may be affected. Elevated inflation and the effects of monetary policy tightening are also restraining domestic consumer demand and business investment. An easing cycle may not begin until the last quarter of 2023 or 2024.

MENA: The region is facing moderate growth slowdown amid oil producers' waning momentum

The MENA region anticipates a moderate reduction in growth compared to the past decade's average, driven by declining momentum in oil producers due to OPEC+ quota cuts. Gulf economies are poised for a significant slowdown, while economic progress varies across countries. North Africa faces challenges due to drought, hampering economic development. Rising interest rates and a sluggish global economy also negatively impact the region.

In the UAE, economic growth is expected to slow in 2023 due to reduced global economic activity, stagnant oil production, and tighter financial conditions. Oil GDP is projected to grow by 2% in 2023, gradually increasing to 2.8% and 3% in 2024 and 2025, respectively. The labor market is cooling with 40 applicants per job opening, up from the pre-pandemic average of 33 applicants. However, hiring shows only a minimal decline of -0.4%, suggesting a relatively stable hiring environment.

In Saudi Arabia, economic growth is set to decelerate from 8.7% in 2022 to 2.9% in 2023 due to stagnant oil production following OPEC+ quotas. Strong oil prices aid credit growth, offsetting tighter monetary conditions on consumption. Notably, hiring in July recorded a significant 29% year-over-year increase.

+++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++

The insights presented in this newsletter were made possible thanks to the work of LinkedIn data scientists Yao Huang, Murat Erer, and Caroline Liongosari.