Despite ongoing global uncertainty and high-profile layoffs, labor markets remain resilient

Head of Economics and Global Labor Markets at LinkedIn

Subscribe to these updates here.

This month's top takeaways:

The Great Reshuffle is morphing into a period of Great Mismatch, where demand for remote work opportunities continues to greatly exceed supply.

Layoffs in media, tech and information continue in a labor market that’s still robust, but slowing rates of hiring suggest that rebalancing in the labor market is under way.

Workers are starting to shelter in place a bit more, as the uncertainty picks up. This is a 180 degree turn from last year when members switching jobs was growing at 50% per year.

Global economic outlook

Global growth has lost momentum amidst high inflation

In nearly all parts of the globe, economies are slowing, high inflation is proving persistent, the uncertainty about the outlook is high, and global financial conditions have tightened significantly amidst the increase in interest rates over the recent months. The prospects for individual major economies in 2023 differ widely.

In the U.S., tightening of monetary policy continues to weaken investment, especially in the housing market. Rising interest rates has also resulted in a strengthening of the dollar, exerting a headwind on export activity. We expect the U.S. economy to slow down further, which could lead to a mild recession in the first half of 2023. However, we don’t expect this recession to be nearly as severe compared to what we saw in 2020 or 2009.

Near-term output declines are projected in many European countries, including Germany, Italy, the United Kingdom and the overall euro area. Europe is being affected particularly heavily by the impact of the war in Ukraine and high energy prices, which are expected to persist throughout 2023.

Higher interest rates, elevated energy and food prices and weak confidence are affecting the United Kingdom, where output is projected to contract in 2023, with tighter fiscal policy restraining the rebound. As in the euro area, weaker demand is projected to help bring inflation down steadily.

Prospects in the Asia/Pacific region, where many countries have relatively low inflation, appear stronger than in the Americas or Europe.

Against the backdrop of slowing global trade and tighter monetary conditions, growth is expected to weaken in 2023 in most other advanced and emerging-market economies, before recovering somewhat in 2024. The slowdown in output growth in 2023 is not generally expected to be reflected in large rises in unemployment.

Hiring continues to slow down after historic highs

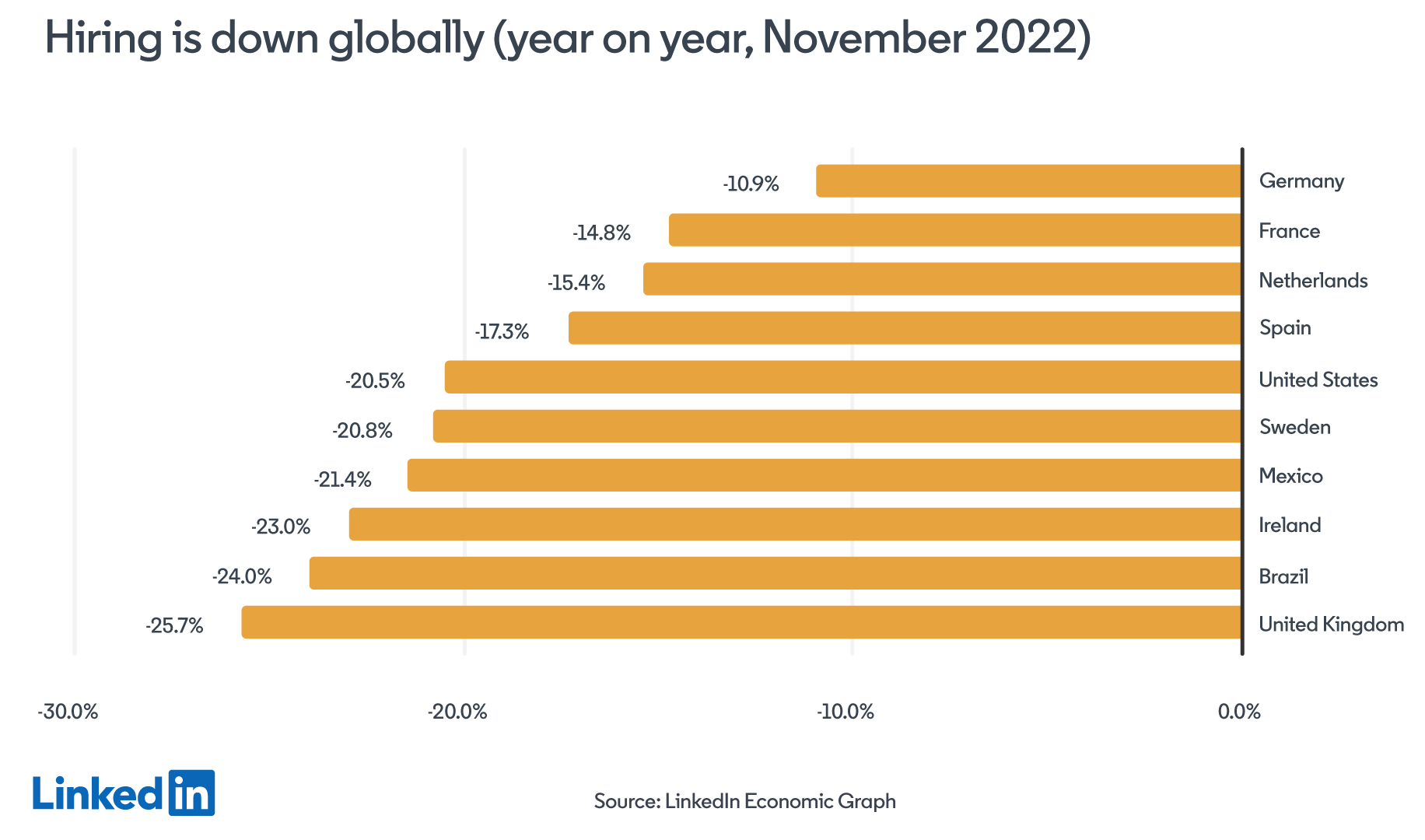

Hiring continued to decline in November 2022 amid increased uncertainty and a slowdown in global economic activity. Relative to November 2021, hiring was down across almost all countries; this was most pronounced in the United Kingdom (-25.7%), Brazil (-24.0%), Ireland (-23.0%), and Mexico (-21.4%). Hiring also slowed significantly in the U.S. as companies have started to tighten their belts and take a more judicious approach to recruiting. However, it is not a one-size fits all experience. For some businesses, the talent squeeze remains as acute as ever. For others, business leaders find themselves rethinking talent needs after a historic year of hiring. Looking across industries in the U.S., accommodation, education, and healthcare are still hiring, while sectors like technology and real estate are especially hurting.

Labor markets around the globe remain robust, but are showing signs of cooling

The global labor market that tightened so much in 2021 has loosened a bit, but still remains tight relative to pre-pandemic levels. LinkedIn’s ratio of job openings to active applicants, our measure of labor market tightness, slowed down in November across most countries, but continues to be nearly double the pre-pandemic average in Germany, the Netherlands, and the U.S.

The Great Reshuffle is morphing into a Great Mismatch

In almost all countries we track, there is a disconnect and a tension between what workers want and what employers are willing to offer when it comes to flexibility and remote work. While remote work appears to have peaked in many countries, workers’ hunger for remote work has not peaked.

The mismatch is especially pronounced in the U.S., where remote job postings shot up from less than 2% in January 2020, peaking at close to 20% of all job postings this past spring. They have since come down to around 14% of all job postings, in a sign that employers are ready to see workers back in the office. On the other hand, of total job applications sent on LinkedIn in November 2022, 52% were for remote positions, up from 50% in the previous month.

In the UK, Sweden, Netherlands, and Germany, the share of remote applications continues to be nearly double the share of remote job postings. This mismatch could last a while, at least until we start seeing a more meaningful cooling down in the labor market. However, there is little evidence so far that employees are willing to give up easily on flexibility.

On the other hand, of total job applications sent on LinkedIn in November 2022, 52% were for remote positions, up from 50 in the previous month. This mismatch could last a while, at least until we start seeing a more meaningful cooling down in the labor market. However, there is little evidence so far that employees are willing to give up easily on flexibility.

U.S. labor market overview

The U.S. labor market still shows signs of resilience despite layoffs and slowdown in hiring

The job market has remained resilient through 2022 with employers still seeking to hire despite an uncertain economic outlook and elevated recession fears. As of December 1, 2022, there was nearly one job opening for every active applicant on LinkedIn. This ratio is double the 3-months average that preceded the pandemic, suggesting that there are still a lot of jobs out there for those looking for work.

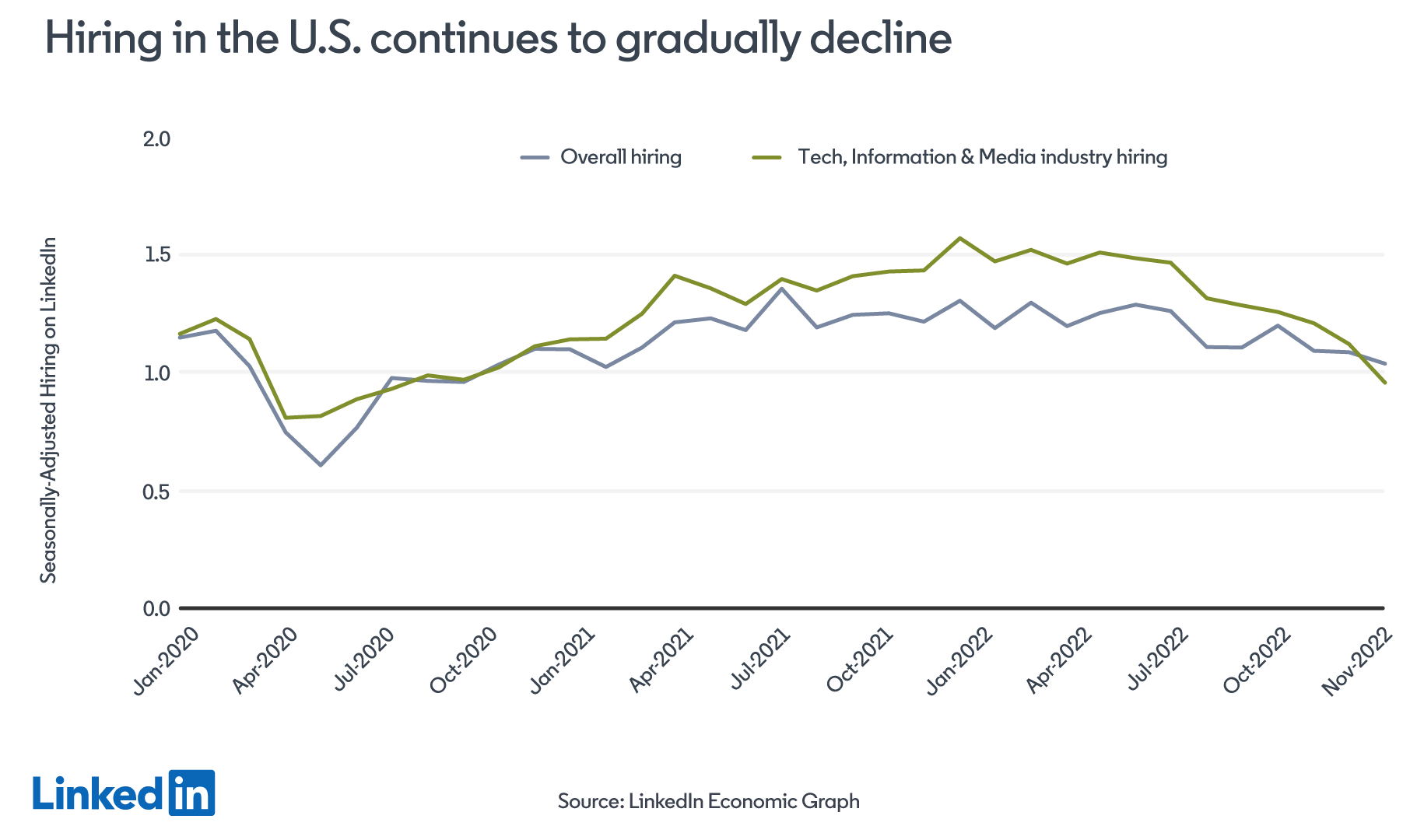

After declining in the Spring, the LinkedIn Hiring Rate held mostly stable during the Summer, but hiring conditions suggest that the labor market is beginning to slow in a more pronounced way across most industries.

With the candidate market cooling down over the recent months, employers are starting to feel they could “ease up” a bit on the breakneck speed with which they had been hiring in previous years. Hiring across the U.S. was 4.9% lower in November compared to last month, and is down 20.5% compared to November 2021. Hiring is now also 11.8% below pre-COVID hiring levels (February 2020). Each of the 20 metros tracked by LinkedIn also showed slowdowns: Miami/Fort Lauderdale, one of the hottest job markets of 2021, saw an 8.1% drop in hires. Hiring in the Tech, Information and Media industry is now at its lowest level since July 2020–a sign of a painful recalibration of a sector that saw massive hiring gains throughout the pandemic.

The technology, information, and media sector is navigating a year of transition

The technology, information, and media industry is adjusting to an era of higher interest rates. But despite the wave of layoffs in this industry, in particular, they may be, in part, a return to more normal hiring levels.

Although lags could be understating the layoffs, overall demand for workers remains strong with workers transitioning to other jobs within and across the industry. The current layoffs could present an opportunity for young-tech startups or other companies in different industries to gain access to new talent in a less competitive market. Our data suggests that nearly 40% workers who made a transition in November out of the technology, information, and media industry moved to another job in the same industry. We also see that some workers are finding a home in other industries, such as professional services (20%) and financial services (7%).

On the other hand, despite negative headlines, technology, information and media turns out to be the industry with the highest promotion rates in 2022. While promotions are down slightly in the U.S. compared to last year, data based on an analysis of more than 140 million active LinkedIn profiles in the U.S. suggests that the tech, information, and media industry outpaced all other industries in the percentage of employees that took a step up in seniority.

The balance of power is starting to level out as economic uncertainty picks up and job competition intensifies

The slowdown in hiring is a sign that the balance of power is starting to shift back to employers. Amid the ongoing uncertainty, we expect a further deceleration in hiring going into 2023, especially in sectors like real estate and tech, which saw significant booms during the pandemic. Competition among job seekers is also intensifying as the pool of available talent is simultaneously being swollen by the influx of former tech and media employees. This is likely to slow down the hiring process further. More resumes in hiring managers’ hands indicates that companies have their pick of candidates, and can afford to hold out for their perfect fit rather than hiring someone who ticks only some of the boxes.

Workers in the U.S. are starting to shelter in place a bit more, as uncertainty picks up

The Great Reshuffle slowed down further in November, with the number of U.S. workers leaving their employers to move into new jobs dropping by 22% y/y compared to November 2021. The slowdown is mainly due to the cooling economy which is making it more difficult for workers to job-hop or quit their jobs without another already lined up. This is a 180 degree turn from last year when members switching jobs was growing at 50% per year.

Some businesses are switching gears by leveraging contract workers, filling cracks in the foundation without bearing the expense of full-time employees

The changing employment landscape is resulting in a growing number of roles for contract work, which provides employers with much needed flexibility during uncertain times. In the past 6 months (May to November 2022), the share of paid job postings for contract positions on LinkedIn – out of all paid job postings in the U.S. – has increased 26% compared to the same 6 month period from the year before. In comparison, the share of job postings for full-time positions have only increased modestly (by 6%) in the past 6 months compared to a year ago.

In the tech, information & media sector specifically, we’ve seen a 36% increase in the share of job postings for contract positions in the past 6 months compared to the same period the year before and a 2% decrease in the share of job posts for full-time positions.

The outlook for the U.S. labor market going forward

The labor market remains resilient as characterized by a very low unemployment rate, 3.7% in November, and a relatively high number of job openings to applicants, roughly one opening for every job seeker looking for a job on LinkedIn.

While slower economic growth and a slowdown in the number of new job openings lend some hope that the Federal Reserve could achieve a soft landing and bring down inflation without much of a spike in unemployment, plenty of headwinds and uncertainty continue to swirl.

Looking ahead, we foresee a number of factors slowing down the economy in 2023. Rising interest rates, persistently elevated inflation, and the diminished level of excess savings will reduce consumer spending. The slowdown in consumer spending will likely depress corporate earnings and profit margins, leading to further contraction in aggregate demand. But even if employers’ hiring appetite fades, the supply of workers seems likely to remain tight in the next few years due to a range of factors such as lower-than-expected population growth, long-term Covid illnesses, early retirements, and a decline in immigration.

With a bleak economic outlook and cost of living crisis, the world of work isn’t likely to go back to the way things were before the pandemic. Without a focus on attracting workers on the sidelines of the labor force, the U.S. and many other countries will continue to struggle in filling long-term demand for years to come.

++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++

This article was updated on November 2, 2023.

Definitions

Hiring Rate. The LinkedIn Hiring Rate (LHR) is the number of LinkedIn members who added a new employer to their profile in the same month the new job began, divided by the total number of LinkedIn members in that country. By only analyzing the timeliest data, we can make month-to-month comparisons and account for any potential lags in members updating their profiles. This number is indexed to the average month in 2016; for example, an index of 1.05 indicates a hiring rate that is 5% higher than the average month in 2016.

Open Job Postings. Open premium job postings (paid job postings by employers) on LinkedIn are counted each day. A 14-day moving average of open job postings is calculated to reduce noise from the daily data. The 14-day moving averages of open job postings are then indexed to February 12th of that year.

Remote Jobs. A “remote job” is defined as one where either the job poster explicitly labeled it as “remote” or if the job contained keywords like “work from home” in the listing. The share of remote jobs is calculated in proportion to all paid job postings. LinkedIn analyzed over 1.5 million paid remote job postings in the United States posted since January 2020.

Short Tenure Rate. The YoY change of the “short tenure rate,” is defined as the fraction of positions that were held for less than a year.

Job Transitions. Job transitions are calculated from updates to LinkedIn profiles when a new job at a different company is created after a previous job has ended. This is divided by LinkedIn membership to account for membership growth. This share is compared to the equivalent time in 2019, before COVID, to benchmark the job transition rate against a more “typical” economic year. Student jobs, side jobs, and internships are not included. Jobs must be created on LinkedIn in the same month of the job start date to account for lag in how members update their profile.

Labor Market Tightness. Tightness is measured as the number of active job openings on LinkedIn divided by the total number of applicants in a given month. We measure active job openings as the stock of open job positions on the last business day of the month multiplied by an index of recruiting intensity. The idea behind recruiting intensity is to measure how actively employers are looking to fill vacant jobs. To quantify that, we follow the method developed by Steven J. Davis, R. Jason Faberman and John Haltiwanger (DFH)—the key idea is that a slack labor market makes it easier for employers to hire in general, so less recruiting effort is required to achieve the same hiring rate. To measure active applicants, we include all individuals applying from within the U.S., and who submit at least one application to a U.S.-based job posting.