July 2023 update: Job seekers’ search intensity is surging amid cooling labor markets

Head of Economics and Global Labor Markets at LinkedIn

Subscribe to these updates here.

Global: Resilient growth, but slowdown still ahead

Global: Resilient growth, but slowdown still ahead

The global economy has surpassed our initial expectations, averting a potential 'stagflation' scenario for the time being.

With the decline in energy prices, headline inflation has surpassed its highest point. However, in key economic regions like the eurozone and the U.S., core inflation (excluding energy and food) has remained persistent. This can be attributed to the gradual recovery of demand following the pandemic. The need for additional central bank rate hikes could potentially force real GDP growth in the U.S. and eurozone either to contract or at least stagnate.

As consumer preferences pivot towards services like travel, hospitality, and events, various sectors of the economy are expected to alternate between contraction and expansion. While the overall economy may avoid a complete recession, certain countries, notably the U.S., may witness successive sectoral recessions as a significant aspect of the narrative in early 2024.

As fear of a possible recession rise, businesses continue to scale back their hiring plans

Amid the uncertain economic outlook, companies globally have scaled back their hiring plans relative to last year. At the same time, labor shortages in numerous countries are leading to increased competition for a limited workforce.

Employers are gradually regaining bargaining power as labor market cools down

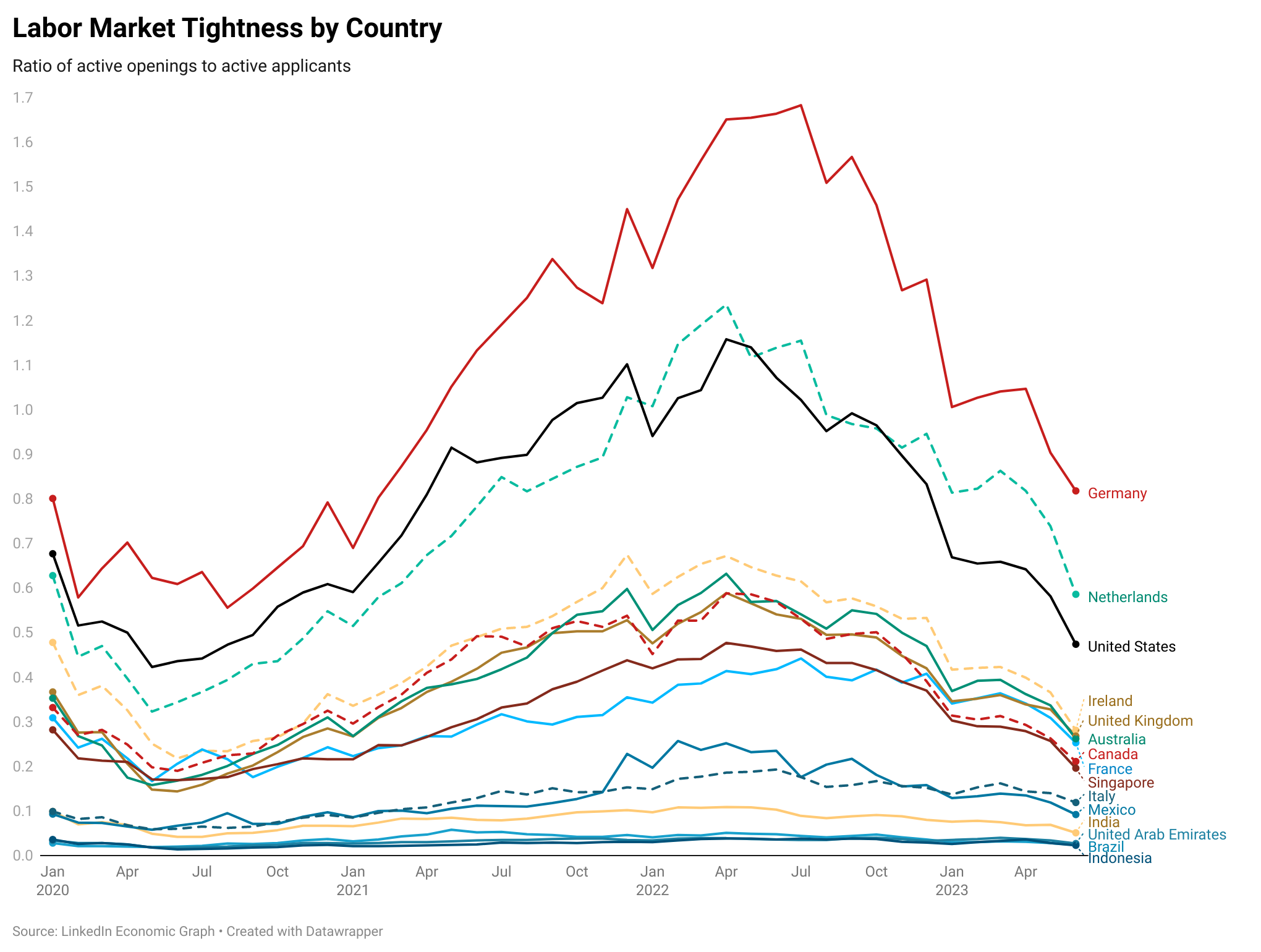

While countries such as the U.S., UK, Canada, India, Ireland, and more recently France are exhibiting increased slack in their labor markets, with LinkedIn's measure of labor market tightness approaching pre-pandemic levels, several European nations like Germany, Italy, and the Netherlands still face tighter conditions compared to their pre-pandemic baseline. This cooling trend implies a potential shift in the balance of power, indicating reduced influence for workers in the job market. As a result, this development will likely contribute to a slowdown in wage pressures.

Job seekers are searching more frequently, realizing that they may no longer have the luxury to take their time

Increased uncertainty in the outlook is leading to a surge in job seekers' search activity. More individuals are actively seeking secure employment opportunities, with some reentering the labor market. Notably, the U.S. has seen a significant 35% year-on-year increase in the number of job applications per applicant on LinkedIn. The United Kingdom, Ireland, and Canada have also experienced notable spikes in job search intensity, with increases of 39%, 30%, and 30% respectively. Italy and India saw more modest increases at 15% and 13% respectively. The UAE, on the other hand, witnessed a slight decrease in search intensity, likely influenced by the summer and vacation season.

U.S.: While still tight, the labor market is cautiously cooling

According to one of the Federal Reserve's key indicators, the ratio of job openings to unemployment, the labor market has begun to show signs of easing. LinkedIn's measure of labor market tightness, which has a slightly different definition than government data (includes all job seekers, not just the unemployed), indicates more slack than government data implies. In June, there was 1 job opening for every 2 active applicants on the platform, marking a significant slowdown compared to the previous peak of 1 job opening per applicant observed in the last months of 2022.

Significant year-over-year hiring declines continue across diverse industries in the U.S.

June 2023 witnessed a 2% decline in hiring across all industries in the U.S. compared to the previous month of May 2023. Furthermore, national hiring in June 2023 experienced a significant 20.9% drop compared to the same period in the previous year, June 2022. However, there are signs that the decline in hiring is starting to stabilize.

The most impacted industry in terms of hiring continues to be the Technology, Information, and Media sector, which saw a staggering 42% decrease in hiring compared to the same period last year. Retail and Wholesale sectors also faced substantial challenges, with YoY hiring rates dropping by 32% each. Real Estate and Equipment Rental Services experienced a 27% decline in hiring, closely followed by Professional Services at 24%. Other industries also faced significant declines, such as Manufacturing and Transportation, Logistics, Supply Chain, and Storage, which both saw a 22% reduction in hiring. Financial Services and Accommodation and Food Services also experienced notable declines at 21% and 19%, respectively.

Workers are staying put amid the global uncertainty

The short tenure rate, or STR, which measures the fraction of positions that end after being held for less than a year, has decreased across industries over the past year.

Short tenures started a growth spell in August 2021 that peaked in March 2022 when the STR was up 10.25% year-over-year. However, due to the current slowdown in the labor market, workers are now staying in their positions for longer durations compared to the previous year, resulting in a year-over-year decrease of -5.46% in STR as of June 2023. This suggests that workers' confidence in the labor market is waning and their expectation to land jobs elsewhere is declining. After all, there are less jobs available for every active job seeker today compared to the trend of the last two years.

Some industries are seeing a more prevalent decline in quick quitting than others, as shown in the chart below above. The STR in the technology, information, and media industry, for example, declined 12.6% year-over-year in June, meaning workers are leaving their jobs at a much slower rate this year compared to last year.

Long distance migrations are on the decline

Migration distances in recent years have exhibited a bimodal pattern, with more individuals moving either short distances (less than 25 miles) or long distances exceeding 3000 miles. This indicates a trend of shorter domestic migrations or movement to and from other countries. It aligns with previous studies highlighting a decline in long-distance migrations, suggesting reduced economic churn and worker reallocation. Additionally, men have consistently migrated farther than women, with men's median migration distance in 2022 being twice that of women's.

Younger generations, specifically Gen Z and Millennials, tend to migrate greater distances compared to older generations. In 2022, Gen Z's median migration distance was 194 miles, while for Gen X it was 34.3 miles. Furthermore, more educated workers tend to migrate longer distances. In 2022, individuals with graduate degrees other than an MBA had the furthest median migration distance (203.5 miles), while those with sub-Bachelor's degrees had the shortest median migration distance (38.9 miles).

Over the past five years, there has been an increase in migrations from principal cities to suburban and rural areas. The share of migrations from principal cities to suburban cores grew by 7.1% from 2019 to 2022, and migrations from principal cities to rural areas increased by 22.38% in the same period. This shift reflects the broader trend of remote work during the pandemic, with people opting to live outside cities. Industries associated with white-collar work, such as Technology, Information and Media, Professional Services, and Financial Services, have witnessed significant migrations from principal cities to suburbs. Popular suburban destinations include Beverly Hills, CA, Frisco, TX, and Leander, TX.

Eurozone: Tight labor market conditions persist in Europe

Despite a challenging global environment, eurozone labor markets remain robust. Recent unemployment for the area came in at 6.5% for May, suggesting the labor market is still tight and employment in the eurozone increased in Q1 2023 by more than it had in the preior two quarters.

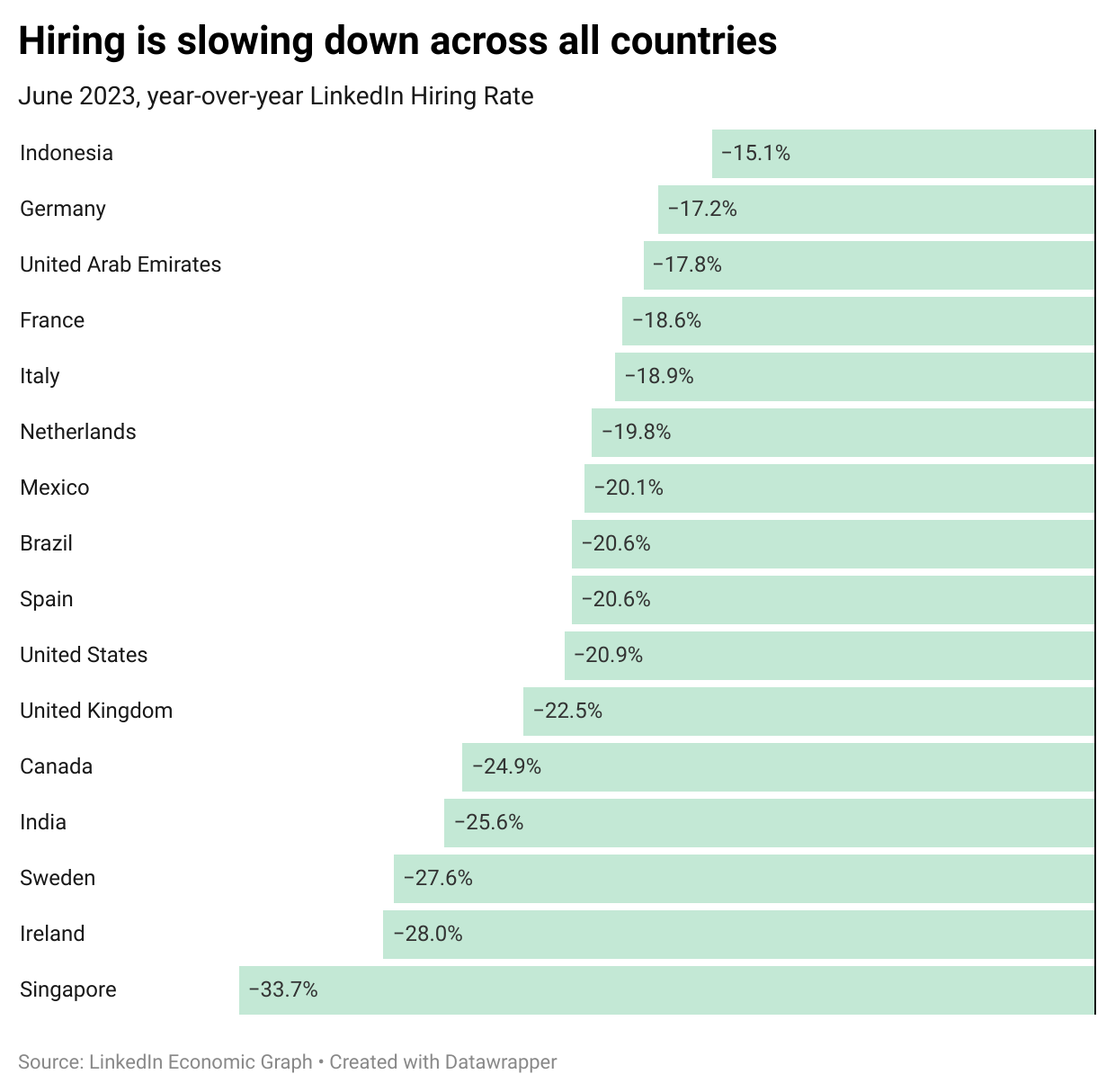

Several European countries, such as Germany, the Netherlands, Spain, France, Sweden, and Ireland, are all witnessing a significant decrease in year-on-year hiring, with declines ranging from 17% to 28%. This decline can be attributed to both economic uncertainty and labor shortages in various industries. Despite this trend, there are still employment opportunities available, as the ratio of job openings to active applicants remains higher than pre-pandemic levels in most countries. Additionally, unemployment rates across Europe are historically low or close to them, indicating a relatively robust labor market. This resilience can be attributed to variations in downturns across different sectors and their timings.

One plausible explanation for the strong labor market is the practice of labor hoarding, wherein companies retain their workforce rather than downsizing during periods of weak demand. This strategy stems from diminishing concerns of a prolonged economic downturn, as businesses anticipate future rebounds in activity and aim to rehire their employees. The scarcity of jobseekers in a tight labor market further intensifies this hoarding behavior, presenting firms with additional challenges in competing for talented individuals.

United Kingdom: Outlook is clouded by prolonged higher interest rates

While UK economic growth has slowed this year, its labor market remains tight. From within this tight labor market emerges continued wage pressure with 3.8% unemployment, and nominal wages accelerating 6.5%.

The UK labor market has seen a significant increase in slack, accompanied by a continuous decline in hiring since the previous summer, indicating reduced demand for workers. Recent data from June 2023 reveals a substantial year-on-year decrease in hiring activity, with a significant decline of 22.5% compared to the corresponding period in the previous year.

Asia Pacific: APAC’s labor markets remain resilient amidst weakening exports and inflation challenges

Australia's labor market remains tight, with four job applicants per job opening in June, reflecting a slowdown from 2022 peaks but still above the early stages of the COVID-19 pandemic. The LinkedIn Hiring Rate is also down by 23% year-over-year. However, weakening domestic conditions pose challenges to the country's economic growth prospects with GDP growth expected to slow in 2023 and 2024 to below trend, thanks to persistent inflation and higher interest rates. Singapore's labor market also exhibits comparable tightness, with nearly five applicants per job opening, aligning with the pre-pandemic average. The LinkedIn Hiring Rate is also down 34% year-over-year, and growth is expected to continue slowing.

In contrast, India is experiencing a more rapid cooling down in its labor market, as there are approximately 20 active applicants for each job opening (compared to 17 last month). Hiring on LinkedIn is down by 26% year-over-year. However, the 2023 GDP growth should falter on the back of weaker trade and accumulative pressures from tighter monetary policy.

LatAm: Brazil’s labor market eases more quickly, while Mexico's is more gradual

Labor market tightness in Brazil has been witnessing a notable slowdown, steadily approaching pre-pandemic levels. This trend indicates an improvement in labor supply along with a gradual decline in openings. On the other hand, Mexico has been experiencing a more gradual transition, with labor market tightness slowly moving closer to its pre-pandemic level.

MENA: While Gulf economies will decelerate the most in 2023, growth remains uneven across countries

The MENA region is projected to experience a slightly slower growth rate in 2023 compared to the average of the previous decade. The momentum of oil producers is expected to decline due to the implementation of OPEC+ quota cuts. While Gulf economies will decelerate the most in 2023, growth remains uneven across country groups. Additionally, North Africa will face challenges due to drought, further impacting its economic progress. The region as a whole will be negatively affected by rising interest rates and a sluggish global economy.

In the UAE, economic growth is projected to slow in 2023 compared to 2022 due to factors such as a decline in global economic activity, stagnant oil production, and tightening financial conditions. Following tighter OPEC+ production quotas, oil GDP is projected to grow by 2% in 2023 and increase to 2.8% and 3% in 2024 and 2025, respectively. Inflation rates are expected to remain subdued at around 3.4% in 2023 due to a stronger U.S. dollar, tighter monetary policy, and falling global commodity prices. Following a period of cooling down, the labor market in the UAE is displaying indications of stability, as year-over-year hiring has decreased by only 17.8%.

In Saudi Arabia, economic growth is projected to slow significantly from 8.7% in 2022 to 2.9% in 2023. Stagnant oil production, as Saudi Arabia adheres to OPEC+ production quotas, will limit oil sector growth. However, the strong oil price backdrop will support credit growth and mitigate the impact of tighter monetary conditions on consumption. Non-oil sectors are expected to grow by 4.1%, offsetting the slower growth in the oil sector. The combination of a relatively strong U.S. dollar, restrictive monetary policy, and controlled domestic fuel prices will keep inflation subdued at 2.4%.

++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++

This article was updated on November 2, 2023.

The insights presented in this newsletter were made possible thanks to the work of LinkedIn data scientists Yao Huang, Murat Erer, and Caroline Liongosari.