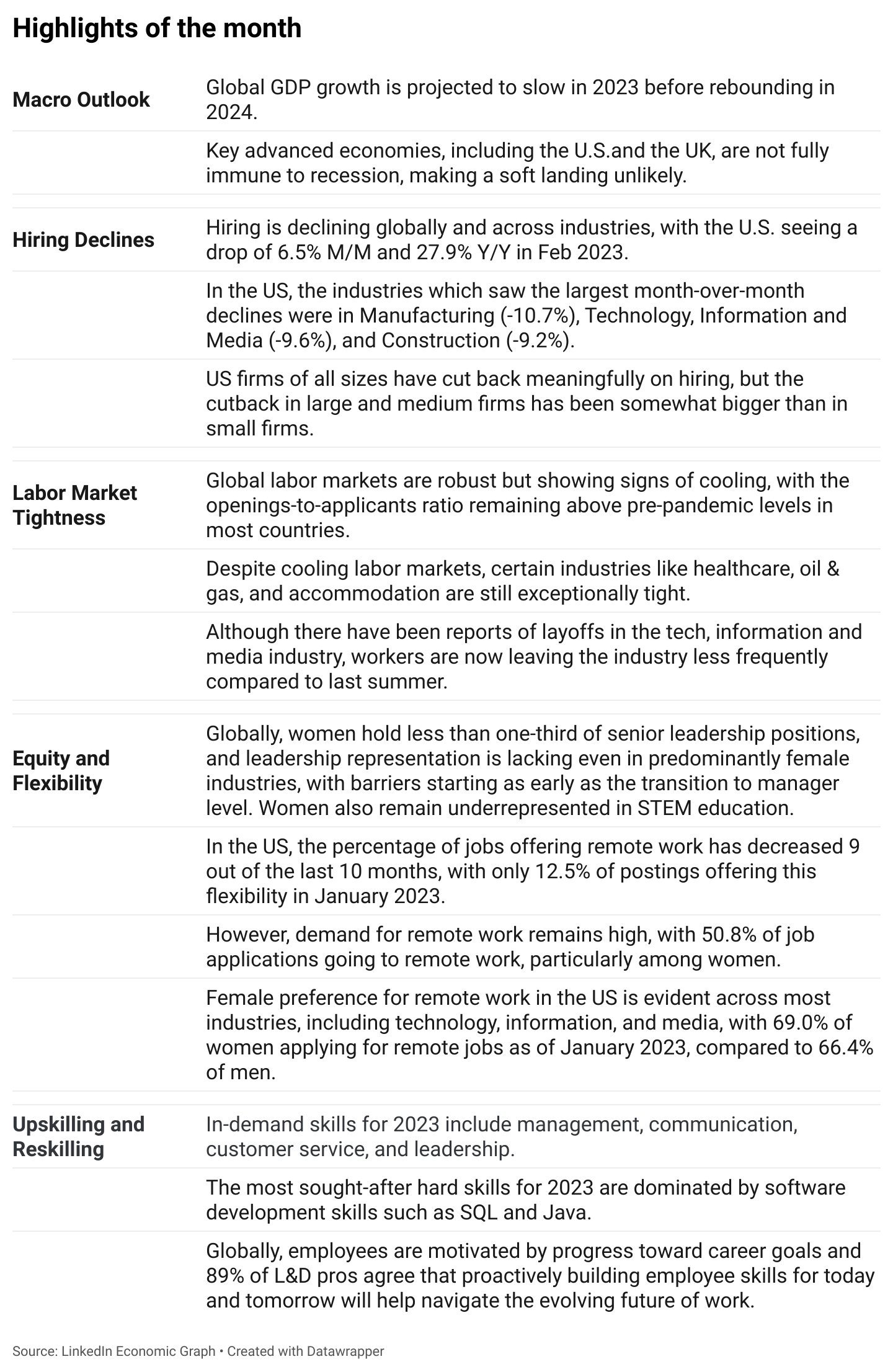

March 2023 update: Weak growth, robust labor markets, and persistent gender inequity

Head of Economics and Global Labor Markets at LinkedIn

Subscribe to these updates here.

Global: A slowdown is anticipated in multiple countries with a subsequent rebound in 2024

Recent economic data suggest that global growth was more robust towards the end of last year than previously projected. Recession concerns among the major economies have subsided in recent months. Not only has global sentiment based on mentions of “recession” on LinkedIn improved, but concerns are also less synchronized across the world. This suggests a better chance of a softer landing for the economy than previously anticipated.

Nonetheless, considerable uncertainty persists regarding the pace at which the magnitude of shocks that have impacted the world will impact the real economy. At present, we are doubtful that the positive surprises observed in Q4 2022 imply that most key advanced economies will entirely evade a recession. Furthermore, the GDP growth in the U.S. and Eurozone seems to be partially attributed to an increase in inventories. In case firms decide to curtail production to lower their inventories to typical levels, this stimulus is likely to be reversed.

Moreover, the complete impact of last year’s policy tightening has not completely manifested in the economic activity. The Federal Reserve and a few other central banks are anticipated to further tighten their policies in the near future, thus we maintain our expectation for a subdued first half of this year for global economic activity.

At present, our assessment is that the latest economic developments support the notion that economies are not on the path towards a significant economic downturn. Global output is projected to slow in 2023, before rebounding in 2024. Key advanced economies, such as the U.S. and the UK, are not fully immune from a recession and therefore achieving a soft landing is not likely to be a possible outcome. The UK is already in recession, so a soft lending there seems very unlikely. In the U.S., achieving a soft landing seems slightly more possible than it did last summer.

We expect inflation to decrease notably across most economies as a result of declining commodity prices, decelerating growth, and alleviating supply chain challenges. However, the speed and pace of decline will vary from economy to economy, contingent upon the extent to which supply and demand factors played a role in propelling inflation in 2021 and 2022.

Despite ongoing challenges, labor markets continue to show resilience

One reason why recession fears have calmed down since the autumn is the ongoing strength of labor markets in different regions of the world. Despite the slowdown in hiring compared to last year, labor markets in most advanced economies continue to defy expectations. While this offers some hope that the expected economic downturn might have a less severe impact on the labor market, it is also probable that this will reaffirm the hawkish stance of many developed nations’ central banks.

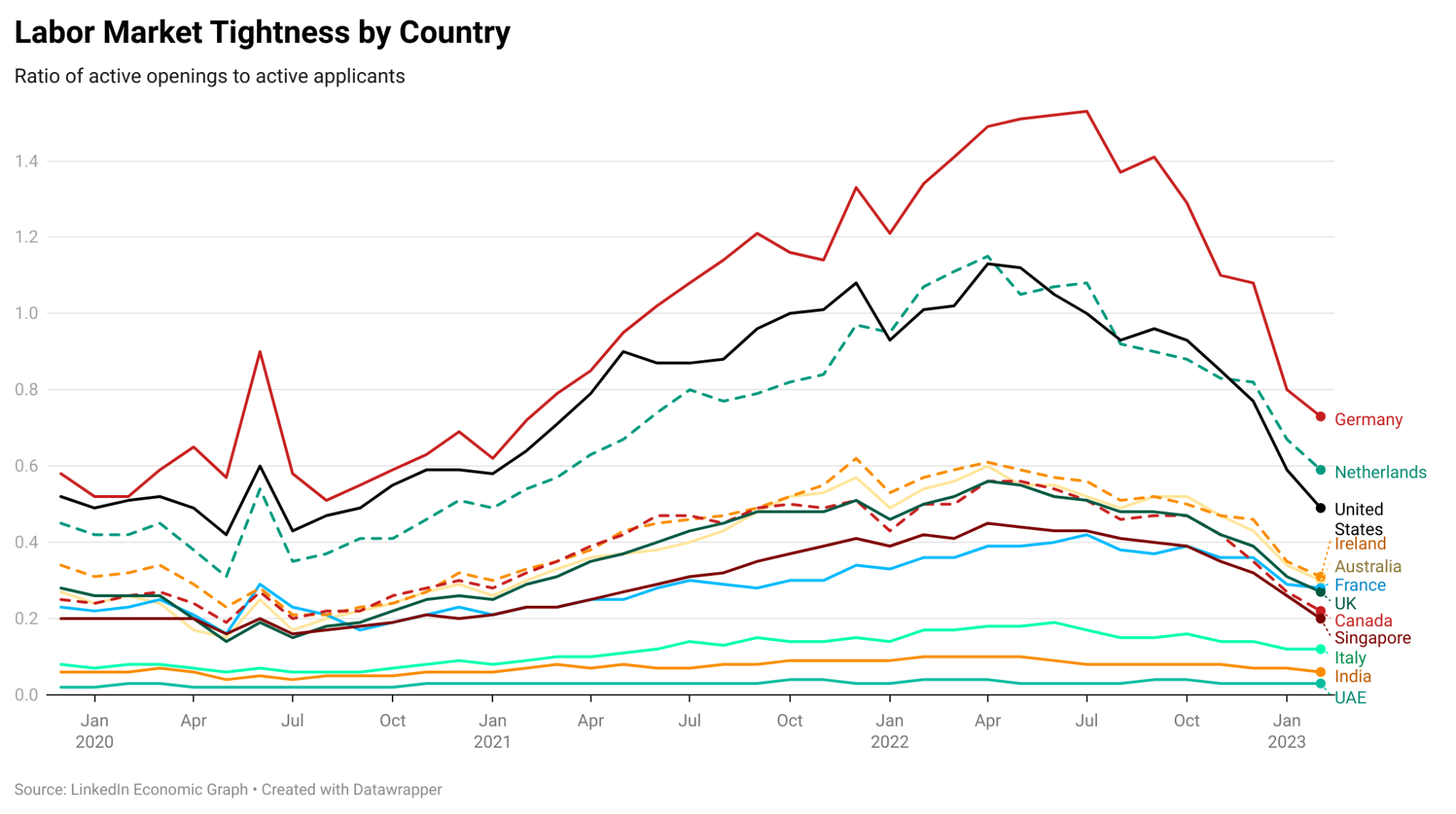

Hiring has been slowing down across all countries, and labor markets have been cooling gradually, albeit remaining resilient in the face of ongoing economic challenges. Uncertainty about the outlook has led companies to scale back their hiring plans, leading to a slowdown of hiring activity in every country. While the ratio of job openings to active applicants, LinkedIn’s measure of labor market tightness, is gradually drifting back to its pre-pandemic normal in several markets, including Canada, Ireland, Singapore, India, UAE, UK, and the US, it remains structurally tight in several European countries, especially Germany, and the Netherlands.

The continuous robustness of the labor market underscores the likelihood that central banks may need to implement more and lengthier monetary policy tightening than was previously forecasted. However, reflecting the diverse employment market landscape, the possibility of additional tightening differs substantially among advanced economies.

U.S.: The labor market showed more signs of cooling in February

The U.S. economy is expected to undergo a moderate recession in mid-2023, due to the restrictive monetary policy of the Federal Reserve and earlier tightening in financial conditions. LinkedIn’s data show that the labor market was showing some signs of cooling at the start 2023. Additionally, gradually weakening employment gains as evidenced by the decline in hiring across the majority of industries in the U.S. mean consumer spending will probably weaken in some part of 2023. We don’t anticipate this recession to result in substantial rise in unemployment compared to what we have seen in 2020 or during the Great Recession.

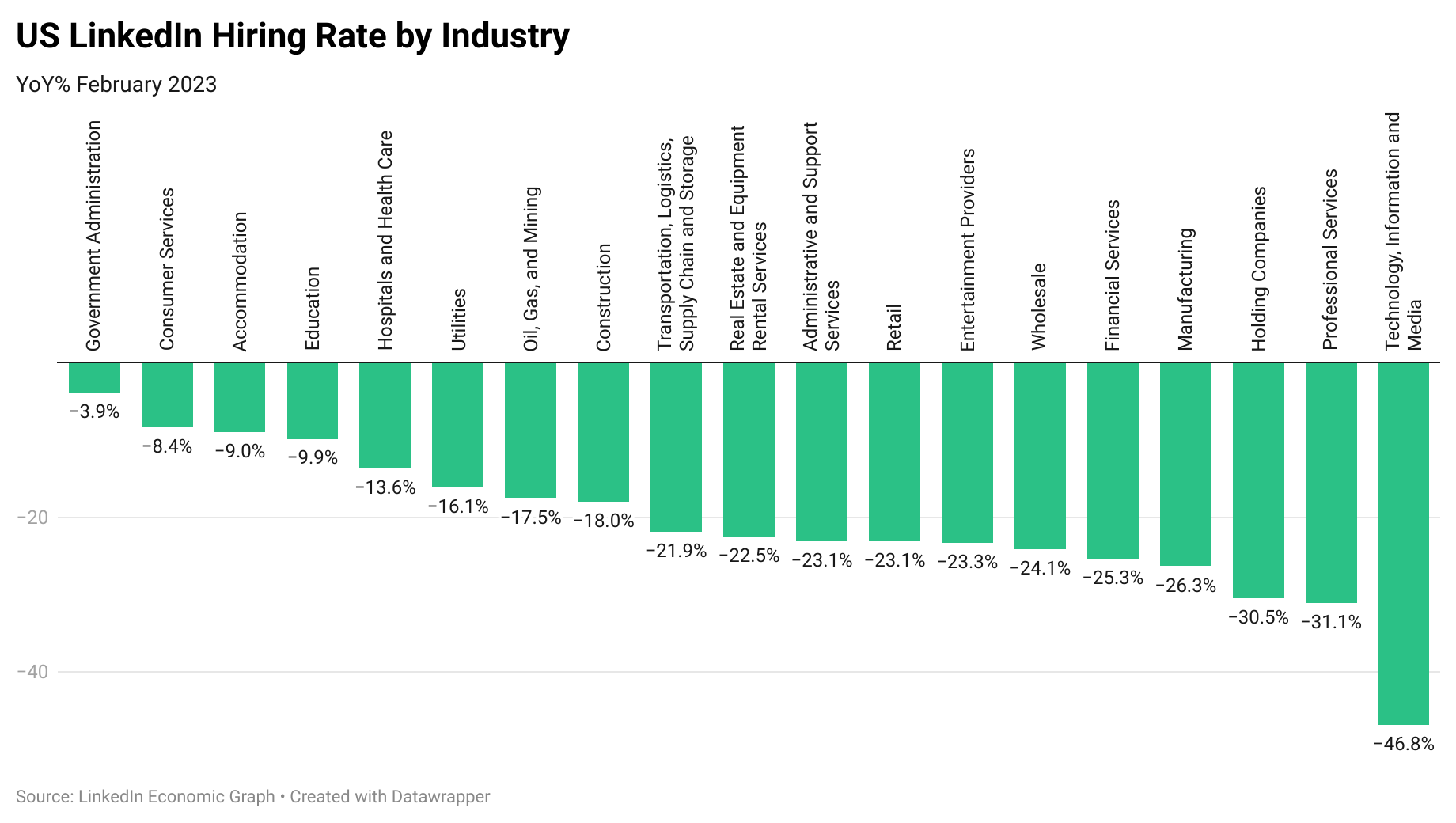

The U.S. labor market saw the largest hiring decline since April 2020, with a 6.5% decrease in hiring across all industries nationwide in February compared to January. Although this is the biggest month-over-month drop seen since April 2020, it’s not anticipated to occur regularly in the future. Hiring has now declined for 10 consecutive months, with a year-over-year decrease of 27.9%.

LinkedIn data from February 2023 also suggests that large and medium sized companies have experienced a somewhat greater decline in hiring year-over-year (YoY) than their smaller counterparts. That is, while all companies have seen a slowdown in hiring, larger ones have been forced to make tough decisions about their workforce, leading to a more significant decrease in hiring activity.

Although employers in all industries have slowed down their hiring, job seekers still prioritize flexibility when looking for employment. In January, paid remote jobs on LinkedIn only represented 12.5% of total job openings, but they received the majority of applications (50.8%) and an outsized proportion of views (43.9%) compared to on-site jobs. While the share of remote job applications has slightly decreased from its peak of 53.2% in July 2022, it is still higher than the 47.5% recorded in January 2022.

Moreover, LinkedIn’s data indicates that women applicants are more likely to apply to remote jobs than men. In January 2023, 54.7% of women in the U.S. who applied to jobs on LinkedIn applied to remote jobs, while only 50.3% of men did –representing a difference of nearly 5 percentage points. This percentage difference has been relatively consistent over time since January 2021. In May 2021, these percentages were 26.9% for women and 21.4% for men.

The slowdown in hiring aligns with the broader trend of cooling labor markets, as shown by the declining ratio of job openings to active applicants ratio since summer 2022. However, this trend is not uniform across all industries. Healthcare, accommodation, and oil and gas are still facing a talent shortage, leading to a competitive hiring environment with the job openings to active applicants ratio above pre-pandemic levels. Employers in these industries are struggling to find qualified candidates to fill open positions. LinkedIn data shows the most-in demand skills that employers are looking for in 2023 include management, communication, customer service and leadership.

In contrast, the financial services, transportation, professional services, entertainment, and technology, information, and media industries continue to cool, with the ratio of job openings to active applicants falling below pre-pandemic levels. Applicants in these industries are applying to multiple jobs before they are hired, and many employers are able to fill vacancies without raising wages.

Moving forward, assuming that our prediction of an economic recession later this year is correct, that resilience in the labor market is unlikely to last. Looking ahead, we anticipate a reduction in domestic demand due to increasing headwinds from tighter financial conditions. We expect this trend to persist in the upcoming quarters as the Fed proceeds with more policy tightening. Labor markets are expected to cool further and wage pressures will diminish, which should help to reduce inflation.

Eurozone: The labor market is showing signs of structural tightness

In the Eurozone, recent positive high-frequency data and an upside surprise in the flash GDP estimate for Q4 2022 have led us to raise our growth forecast, although the overall outlook is still expected to see a fall in Q1, followed by a modest recovery. Some countries, such as France, Ireland, Italy, the Netherlands, Spain, and Switzerland, are expected to see some mild gains in GDP, while Germany, Finland, and Sweden are expected to experience a contraction.

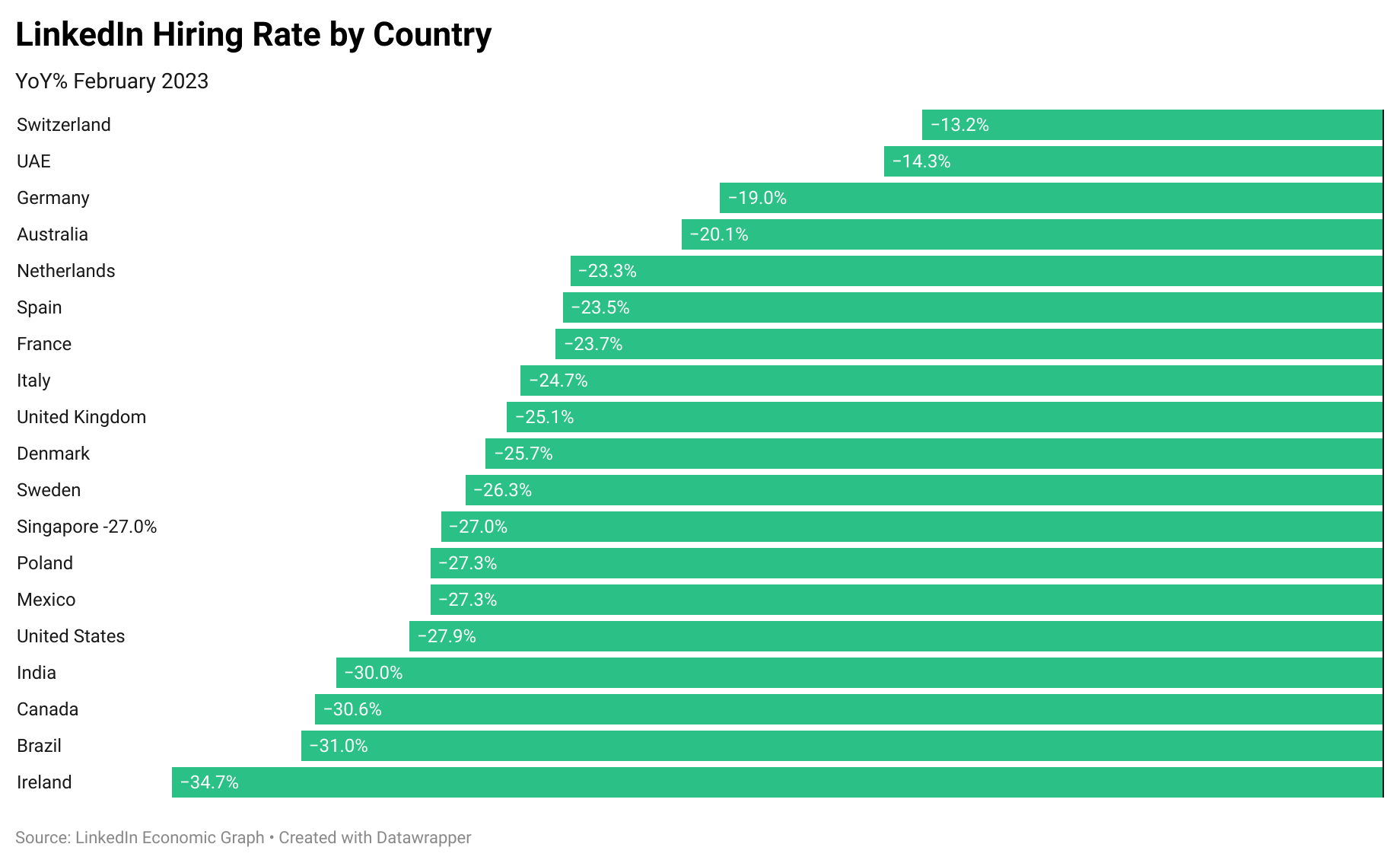

Almost all European countries are experiencing a significant slowdown in hiring year-on-year, including Germany (-19% YoY), the Netherlands (-23.3% YoY), Spain (-23.5% YoY), France (-23.7% YoY), Italy (-24.7% YoY), Sweden (-26.3% YoY), and Ireland (34.7% YoY). Economic uncertainty has played a significant role in this trend, leading to a decline in business activity and a decrease in demand for talent across various industries. However, despite the sluggish economic conditions, LinkedIn’s data continue to point to labor market resilience. In most countries, the ratio of job openings to active applicants remains higher than pre-pandemic levels, and unemployment rates are either at or near historically low levels, both at the national level and across the entire bloc. The ongoing resilience coupled with sticky core inflation numbers is likely going to reaffirm the ECB’s hawkish resolve in tightening policy further.

Looking ahead, we anticipate that hiring will remain stagnant this year, mirroring the growth of GDP. This does not indicate a deterioration in the job market, but rather reflects the resilience of employment during the low phase of economic activity. Therefore, when the economy eventually recovers, the increase in employment will not be as significant. Furthermore, recent gas price developments signal further solid declines to energy inflation, which will continue to push overall inflation lower.

UK: There are growing indications that the demand for workers is declining

In the UK, the bigger picture remains one of the economy enduring a relatively shallow recession in 2023, as tight policy settings and falling real household income are likely to drag down economic activity. While inflation is predicted to have already peaked, it is expected to remain stubbornly high throughout 2023.

The latest data indicates that what was once an extremely vibrant job market is now showing signs of slowing down. Although job openings were still high in Q4 2022, there has been a continued decline in hiring since last summer, indicating a decreasing demand for UK workers. More recent data from February 2023 reveals a significant YoY decline in hiring activity, with a sharp 25 percent decrease compared to the same period last year. But the recent unprecedented tightness of the labor market should limit how far unemployment rises in the recession we expect the economy to endure this year. The ratio of job openings to active applicants is still higher than its pre-pandemic average.

The labor market is expected to recover slowly, with labor supply being slow to catch up. Although labor market conditions are likely to loosen somewhat, unemployment is expected to peak much lower than in previous economic cycles.

Asia Pacific: Labor markets are cooling, without a rise in unemployment

While APAC is still growing at a comparatively stronger pace than the rest of the world, the region is not immune to the global headwinds which will exert some pressure on its growth.

High inflation and global economic slowdowns are resulting in slowed growth in APAC, and our data shows that hiring has started to level off after the historic highs in early 2022. Singapore and India have both experienced a substantial slowdown in hiring YoY, with a decline of 27% and 30.6%, respectively, in February 2023. This trend can be attributed to a variety of factors, including increased economic uncertainty and shifting market conditions. Australia has seen a slightly lower decline, with hiring slowing down by 20.1% YoY.

The ratio of job openings to active applicants, LinkedIn’s measure of labor market tightness, is cooling back to pre-pandemic levels. Australia and Singapore have similar levels of tightness, with 4 and 5 active applicants per job opening respectively. India shows slightly more competition for jobs, with 16 active applicants per job opening. At the same time, however, based on government statistics, unemployment rates are currently at 50-year lows. This indicates that jobseekers, while still employed, are still looking for other roles.

The combination of low unemployment and a labor market back at pre-pandemic levels of tightness, together, suggest that the cooling that we have seen over the past quarter is likely to slow in the coming months as the markets approach equilibrium.

Latin America: The region’s labor market face a complex and uncertain future

The economic outlook for Latin America appears challenging, with many economies in the region likely to experience a mild recession in 2023. Inflation, however, is a bright spot, as it has already peaked in most LatAm economies, and central banks are expected to begin cutting rates as early as Q3 2023.

Brazil has been successful in reducing inflation by more than half between June and December of last year, due to a hawkish monetary policy. However, the country has experienced a significant slowdown in hiring, with a 31 percent decrease in February 2023 compared to the same period last year. On the positive side, unemployment remains low and has reached its lowest level since 2015.

Gulf Cooperation Council: The labor market outlook for the GCC region appears more upbeat in comparison to the rest of the world

After an impressive year in 2022, the economies of the Gulf Cooperation Council (GCC) are expected to slow somewhat in the coming months. However, the region's GDP is predicted to grow at a rate more than twice that of the global economy. Although the oil sector is projected to stagnate due to OPEC+ production cuts, growth in the non-oil sector is expected to hold up much better. While the oil price has eased, it is expected to remain supportive of GCC budgets. Inflation in the GCC is predicted to ease somewhat but remain higher than the global average.

In the UAE, economic growth is expected to ease this year, but momentum remains solid. Hiring slowed down in February by 14.3% compared to the same month last year and the impact of higher interest rates and potential recessions elsewhere in the world will likely weigh on further on the labor market in H1 2023. However, the government’s growth and diversification agenda will provide an important cushion to the economy.

In Focus: Women representation in leadership is low

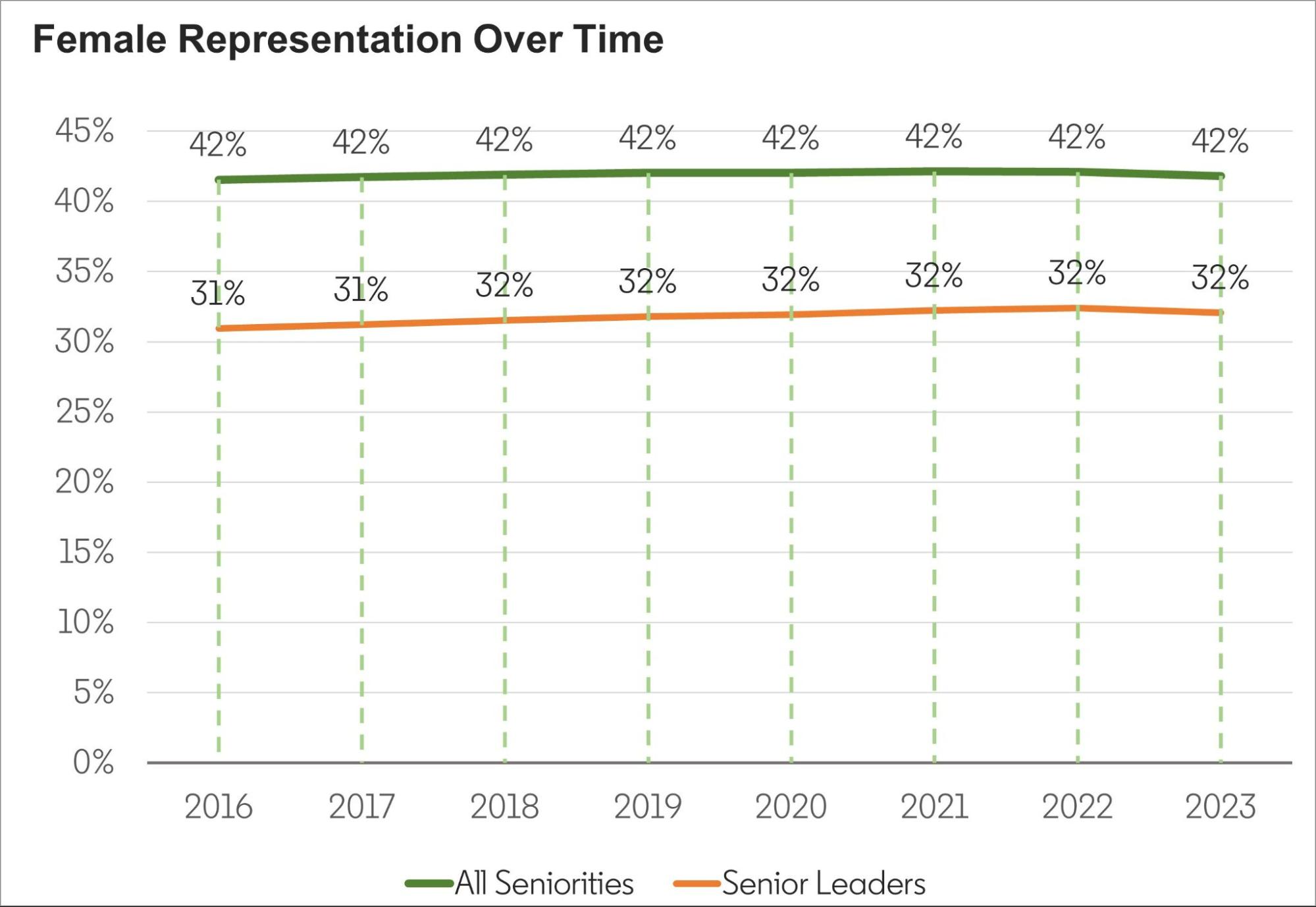

New ata from LinkedIn reveals that women continue to be underrepresented in leadership positions worldwide, even in industries where female representation is comparatively high. Merely 32% of leadership roles are occupied by women globally, indicating the persistent gap in gender parity in leadership. Moreover, the data also emphasizes the sluggish progress towards closing this gap, as the proportion of women in leadership positions has only increased by 1 percentage point since 2016. These trends are reflected across North America, Asia Pacific, and Eurozone and Latin America regions.

The gender gap in leadership positions is not only evident in the under-representation of women in leadership roles but also in the disproportionate decline of women as they progress up the ranks. The proportion of women in leadership positions declines as they move up the leadership ladder, with the most significant drop occurring between the Senior contributor and Manager levels. These findings highlight the need to address the challenges and barriers that impede women’s advancement from the early stages of their career and to create a more inclusive and equitable environment that promotes diversity and gender equality in leadership positions.

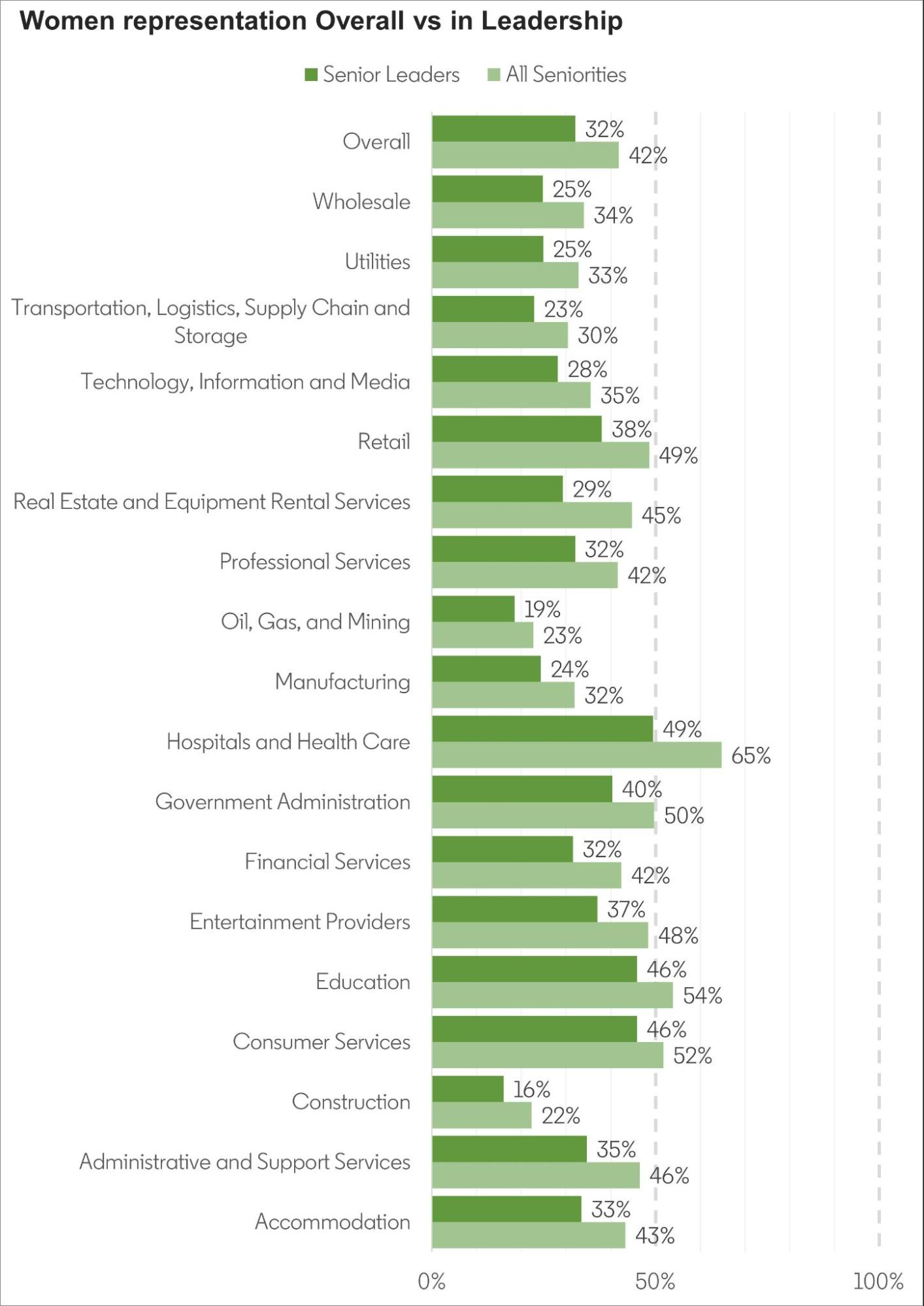

Furthermore, the gender gap in leadership roles is prevalent across various industries, with significant disparities between women’s representation overall and their representation in leadership positions. For instance, while women represent nearly 46% of the workforce in the Administrative and Support Services industry, they only occupy 35% of leadership positions worldwide. However, the magnitude of the gap varies across industries. In sectors such as healthcare, women’s representation in leadership is higher than in other industries, but it is still far from women’s overall representation. Conversely, in male-dominated fields such as technology and finance, women’s representation overall and in leadership roles is comparatively low.

Finally, women continue to be underrepresented in STEM education and careers. LinkedIn’s research analyzing millions of profiles in the U.S. show a significant gender gap exists in both the rate of holding STEM skills and in STEM employment. The research also shows that the greatest expansion in the gender gap occurs between obtaining a STEM degree and working in STEM one year after graduation. During this timeframe, the gender gap in STEM widens by ten percentage points.

+++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++

This article was updated on November 2, 2023.

Insights on gender representation presented in this newsletter were made possible through the research conducted by Silvia Lara, Rosie Hood, Matthew Baird, and Caroline Liongosari.