May 2023 update: Immaculate cooling persists across labor markets globally, but abundant bright spots shine through

Head of Economics and Global Labor Markets at LinkedIn

Subscribe to these updates here.

Global Landscape: Recent banking turmoil has not derailed the outlook

While the recent stress in the banking sector could provoke a global recession, we see this as unlikely. The primary route through which we anticipate issues within the banking system to affect the worldwide economy is through further tightening of credit conditions for both consumers and businesses. Further tightening of credit conditions may significantly affect activity and therefore we expect growth to be more subdued over the remainder of this year.

At a global level, we predict that the expected moderate quarter-to-quarter GDP growth rates of 2023 will persist throughout the first half of 2024. We also expect lagged effects of monetary policy tightening to curtail growth in 2023. We expect the slowdown in growth will be particularly acute in H2 of this year as it’s expected the US will enter into a recession for the remainder of the year, while growth will remain modest in Europe and Latin America, and we expect solid growth in APAC and the MENA regions. While we were previously expecting a mild recession in the UK, that is no longer the case. Instead, we now expect very slow positive growth, comparable to continental Europe.

Headline inflation in the US and Europe remains at a high level and there is a continued momentum in core inflation, which is being supported by positive news from the real economy. This suggests central banks are unlikely to cut rates soon. However, headline inflation is expected to fall significantly in the coming months on the back of much lower energy prices and continued easing of supply bottlenecks.

Employers are slowly regaining the upper hand in the labor market

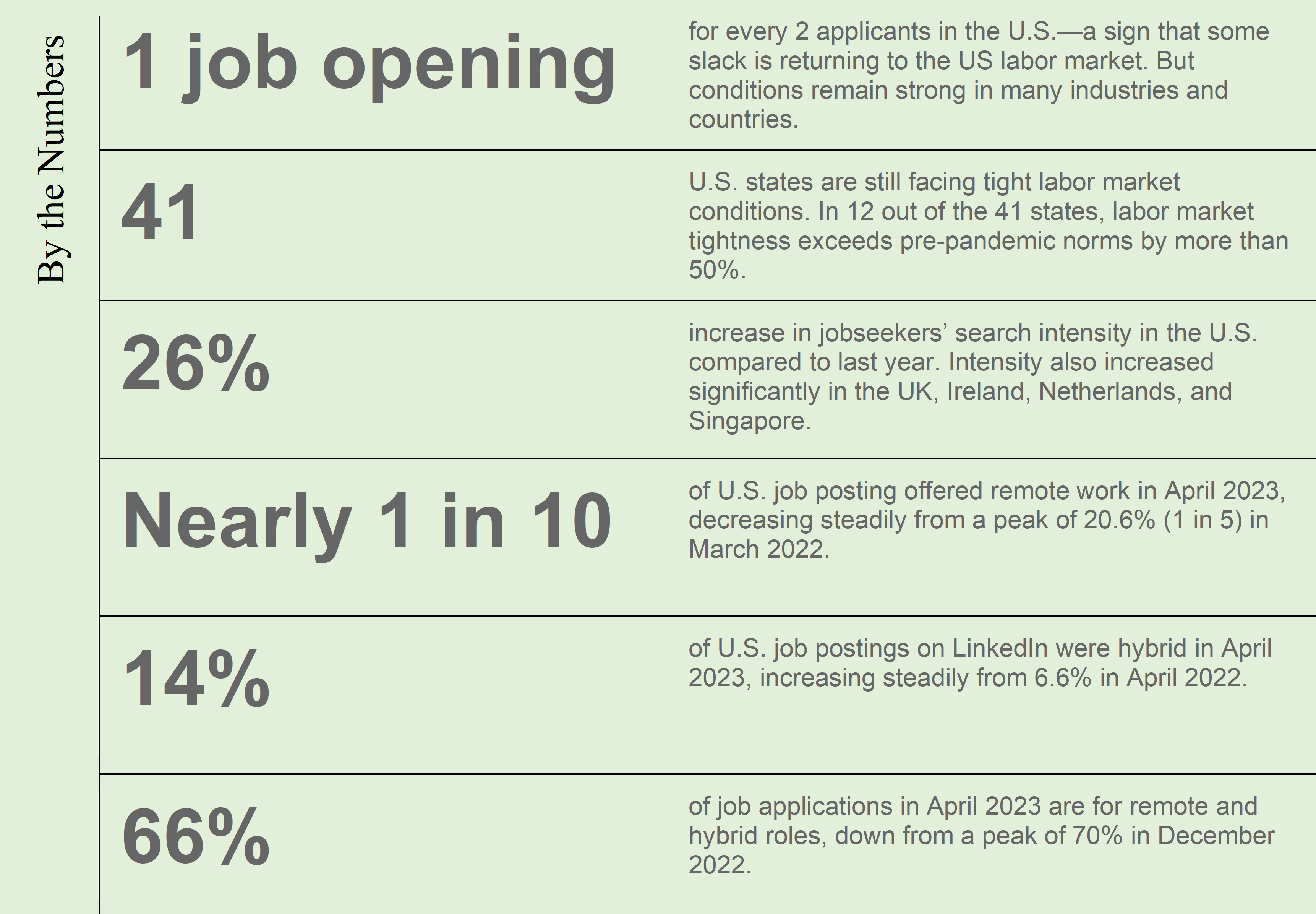

The ratio of job openings to active applicants, LinkedIn’s measure of labor market tightness, is gradually returning to pre-pandemic levels in several countries, such as the US, UK, Canada, India, Ireland, and Singapore. This indicates that slack is reappearing in the job market in these countries. The cooling is also a sign that workers are losing some of their previous power in the job market and, thus, we could see some downward pressure on wage demand and inflation.

Several European countries, including Germany, France, Italy, and the Netherlands continue to have job openings to active applicants ratio that is higher than their pre-pandemic baseline. This is likely due to a combination of worker shortages and higher-than-average number of job openings.

Moreover, the widespread reports of layoffs have resulted in a significant increase in job seekers’ search intensity. People are now actively seeking more stable employment, and many who had stayed on the sidelines for a while are now rejoining the labor market. In the US, the number of job applications per applicant on LinkedIn has increased by 26% year-on-year. In addition, job search intensity has increased by 31% in the UK, 28% in Ireland , and 27% in the Netherlands. The increase was smaller in Australia, Canada and Germany, at 22%.

US: The labor market is cooling, but conditions vary by industry and state

The US labor market continues to exhibit remarkable resilience, with job openings remaining above their pre-pandemic levels. This points to a robust demand for workers in certain sectors, although in some pockets of the economy cracks are appearing. Labor shortages remain the main challenge for employers and the hiring frenzy we saw over the past two years has been fading out.

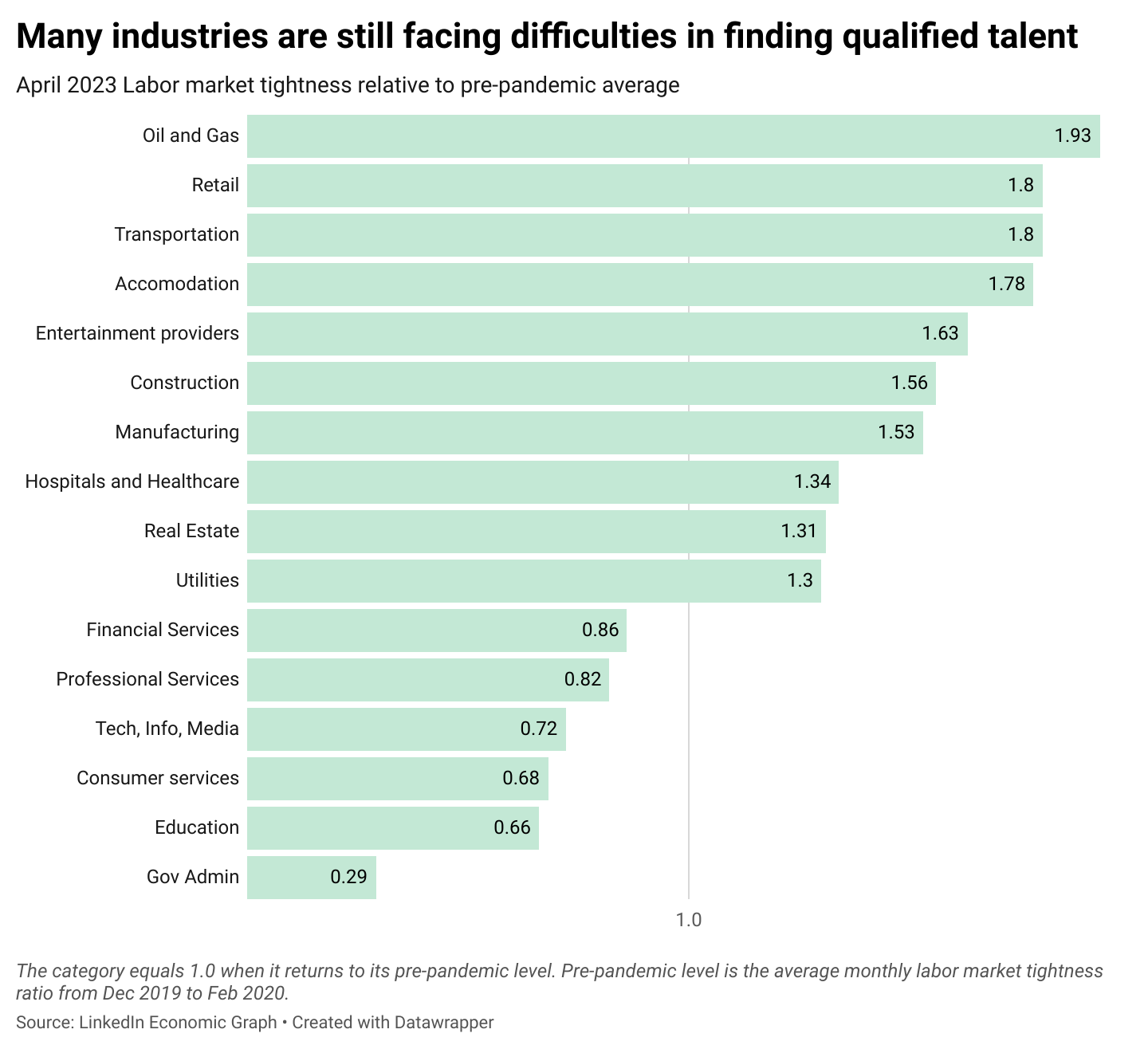

The big picture: There are still many more job openings now than there were in February 2020, and employers in some industries are still struggling to find talent.

Compared to the pre-pandemic era, labor market conditions in industries such as oil and gas, retail, transportation, accommodation, entertainment providers, construction, and manufacturing are still very tight. Employers in these sectors are struggling to find qualified candidates to fill available positions, resulting in a highly competitive environment where the job openings to active applicants ratio exceeds pre-pandemic levels. The steady demand for workers in the accommodation sector highlights the underlying strength in an industry defined by people spending vacations, hotel stays, and restaurants.

In contrast, job seekers in industries such as government administration, consumer services, education, technology, information and media, professional services, and financial services are often applying for multiple jobs before securing one. As a result, employers in these sectors have been able to fill vacancies without increasing wages. These industries are currently experiencing a slowdown, with the ratio of job openings to active applicants dropping below pre-pandemic levels.

Labor markets are cooling, but experiences at the state level are not uniform

Despite the labor market cooling observed at the aggregate national level, a disaggregated state-by-state view suggests a more uneven pace of cooling across the US. Below, we adopted an approach first employed in a paper by the Kansas City Fed using LinkedIn data to explore differences in these conditions using LinkedIn’s ratio of job openings to active applicants. We show that the intensity of the strength of the recovery varies geographically when compared to the pre-pandemic norms in each state.

The chart below shows the evolution in labor market tightness for all US states (including Washington, D.C.) from February 2020 to April 2023. In 41 states, labor markets are still tighter than they were before the pandemic. That is, from the perspective of job seekers, there is an abundance of jobs available for those looking to work when compared to pre-pandemic norms. In 12 out of the 41 states, labor market tightness exceeds pre-pandemic levels by more than 50 percent, with the most significant uptick in Louisiana (+74 percent), Michigan (+65 percent), and Alaska (+63 percent). Conversely, labor markets in 10 states (including D.C.) are less tight than they were before the pandemic, though the gap for most states is relatively small. In these cases, there is an abundance of job seekers competing for available jobs.

Overall, as with the Kansas City Fed’s original finding, the chart above suggests sizable variation across US states in terms of the labor market cooling down. In certain states, the disparity between the demand for talent and its supply has substantially widened since the pre-pandemic era. To address this imbalance, employers can provide more flexibility, such as offering remote work arrangements and upskilling opportunities, which are among the top priorities for job seekers today. By doing so, employers can mitigate spatial mismatch and distribute economic opportunity more evenly across different regions, rather than concentrating it in a few areas and exacerbating the existing imbalances.

Nearly 70% of job seekers are keen to find remote and hybrid opportunities

Despite cooling labor markets, a remarkable 66% of applications on LinkedIn are going to jobs that offer the option to work from home for all or part of the week. Further, 46.5% of applications are from job seekers who want to work only remotely, and 19.5% are from those who prefer to work most of the time remotely. Job seekers’ preferences to work remotely remained quite stable throughout the year.

Gaps between preferences for flexible work and opportunities persist

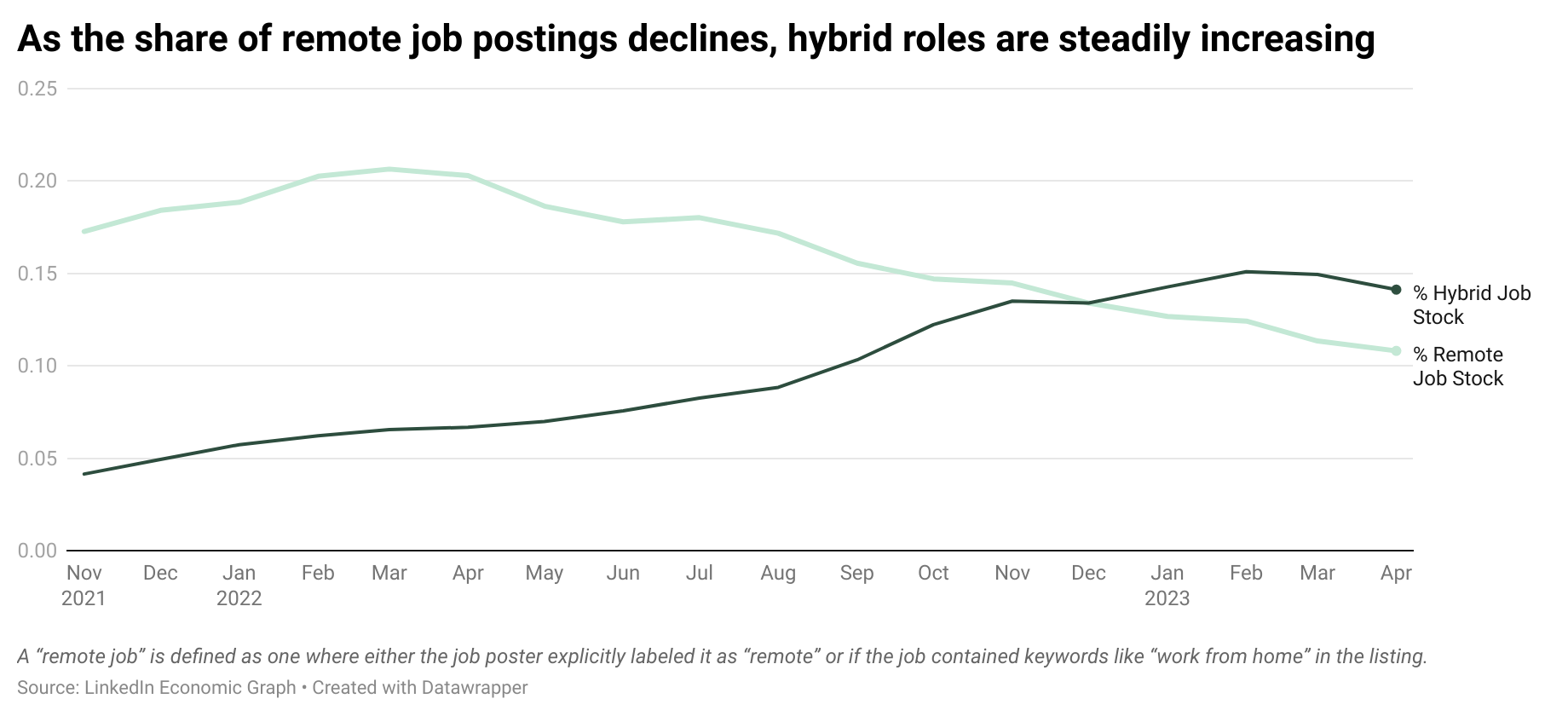

Despite job seekers continuing to embrace flexible work and demanding more of it every month, the availability of these roles has been steadily decreasing. In April, the proportion of job postings offering remote work in the US reached 10.8%, down from a peak of 20.7%. On the other hand, hybrid roles are on the rise, where in April we saw an increase in the availability of these roles to 14%, up from 6.6% in April 2022.

Nevertheless, with tightness persisting in some industries, employers are still considering how to meet workers’ desire for flexibility in different ways.

Remote work is challenging and reversing in certain industries

Remote work is not feasible for some major industries, such as transportation, accommodation, and manufacturing. This is because many tasks in these sectors require physical presence or interaction with customers. These industries were also among the hardest hit during the pandemic, as the goods and services could not be provided virtually. As a result, they faced significant challenges with employee and revenue loss.

While remote work has become more common in recent years, there are still some industries where it presents a challenge. Some businesses in these industries may have adopted remote work as a temporary measure, but many are now returning to an in-person work environment. As of April 2023, the industries with the highest percentage of job openings that require on-site work include Accommodation (83.1%), Real Estate (79.4%) Farming (78.1%), and Government Administration (73.8%) .

On the other hand, Technology, Information and Media (26.3%) , Professional Services (21.6%), Education (17.6%) are the industries with the highest percentage of paid job postings that offer remote work. Furthermore, the top three industries for hybrid job postings are markedly different, with Professional Services (32.8%), Construction (23.4%) and Financial Services (22.5%), taking the lead.

Gen Zers and millennials split over the appeal of remote work

While the majority (66%) of job seekers are interested in fully remote or hybrid work, this sentiment is not shared equally among all generations. Our data suggests that Gen Z employees are less interested in remote work options. They are the least likely among all workforce generations to apply for remote work, and are more likely to apply for hybrid roles. As of April 2023, only 36% of Gen Z job seekers in the US were applying to remote jobs, compared to 50.6% of Millennials and 52.5% of Gen X. On the other hand, only 17% of Gen X job seekers were applying to hybrid roles, followed by 19.2% of Millennials and 22.2% of Gen Z.

Remote work leads to more and better matches

Proximity to work used to be a significant consideration when job hunting, but with remote work, physical distance is no longer a barrier. Previously, long-distance candidates were often ignored, as distance posed challenges for commuting. However, converting in-person roles to remote positions expands the talent pool significantly. We do observe differences across industries in terms of the opportunity to work flexibly and points to certain segments where companies must compete for talent. For example, the accommodation industry, where conditions are still tight by historical standards, is one of the industries with the lowest ratio of remote-work options.

Eurozone: Labor market conditions in Europe continue to be tight

Based on the latest data, the Eurozone economy had a sluggish start in 2023. National Q1 GDP numbers were mixed, with Germany experiencing no growth, France having moderate growth, and Italy, Spain, and Portugal having robust expansions. However, what was common across these countries was the strong performance of net exports, reflecting good export growth and weak imports. This is likely due to a stronger-than-expected start for the Eurozone industry in 2023, with the easing of supply bottlenecks, lower energy prices, and some global economic resilience providing some relief to the sector. We continue to expect the rest of the year to be subdued.

Besides the uncertainty surrounding energy prices and the war in Ukraine, it remains unclear how the current monetary tightening will affect the economy, especially since the ECB is still raising rates at a significant pace. Most European countries are experiencing a cooling in their labor markets, with Germany’s labor market tightness down by 50% YoY, the Netherlands by -46% YoY, France by -60% YoY, Italy by -37% YoY, and Ireland by -53% YoY. Economic uncertainty has played a significant role in this trend, causing a decline in business activity and a decrease in demand for talent across various industries.

Although there has been a noticeable decrease in headline inflation, it still remains at a very high level. Additionally, core inflation momentum remains elevated amid positive news from the real economy.

UK: The outlook for this year has been improved due to positive revisions made to historical data

Although there has been a slight increase in the unemployment rate and a decrease in job openings, we’re not expecting any significant increase in the unemployment rate. This is driven by an improved GDP outlook and the probability that some companies will choose to keep employees rather than downsizing due to difficulty in recruiting talent, However, we expect that tighter financial and credit conditions caused by the banking sector's pressures will adversely affect economic activity in the coming year.

Recent data indicates that the once-thriving job market is now showing signs of a slowdown. Although job openings remained high in Q4 2022, hiring has been steadily declining since last summer, indicating reduced demand for UK workers. Data from April 2023 shows a significant year-on-year decrease in the labor market tightness metric, with a sharp -54% decline compared to the same period last year, returning to the pre-pandemic levels.

Asia Pacific: Labor market conditions in the APAC region are displaying signs of continued loosening

The Asia Pacific region is expected to grow in 2023, primarily due to an upgrade to Chinese GDP growth. However, there are concerns for the second half of the year, as well as for 2024, as global growth momentum diminishes and the initial boost from reopening in China subsides.

There are some indications of loosening labor market conditions. LinkedIn’s job openings to active applicants ratio, a measure of labor market tightness, is approaching pre-pandemic levels in the APAC region. In Australia, labor market tightness declined by -51% YoY, and data from April 2023 suggests that there are now approximately three active job seekers competing for each job opening. In Singapore, there is slightly more slack in the labor market, with five active applicants per job, a -55% YoY decline compared to April of last year. In India, conditions are also slowing down, with the ratio of job openings to active applicants ratio declining by -50% YoY, with 17 active applicants competing for each job opening in April 2023. However, based on government statistics, unemployment rates are currently at their lowest level in 50 years, suggesting that employed individuals are searching for alternative employment opportunities.

LatAm: Latin America faces economic slowdown despite slight improvement

Latin America's economic prospects have improved slightly, but the region will inevitably continue to face lower momentum this year. We continue to expect the region to enter a mild recession in Q2 this year, although conditions will vary across countries. Both Mexico and Brazil are likely to avoid a recession in H1 2023, supported by a boost in services activity and fiscal expenditures. In addition, due to persistent inflation, central banks are likely to avoid cutting rates too quickly or prematurely, meaning that monetary policy is expected to remain restrictive throughout 2023.

Gulf Cooperation Council: Labor market outlook for the GCC region remains positive despite slowdown in growth

While the economic situation in the GCC region remains better than the global trends, its GDP growth rate is expected to drop by more than half to 2.5% this year from 5.1% in the previous year. This deceleration is likely to worsen due to reduced oil production and the implementation of more stringent policies. The rise in interest rates and recession fears from other parts of the world is weighing on consumption and private investment in UAE and the recent OPEC+ policy will drive a further slowdown in growth. Labor market conditions slowed down in the UAE, with the ratio of job openings to active applicants declined by -27% YoY in April 2023. Similarly, we expect growth in Saudi Arabia to ease amidst a weaker global environment and further cuts to oil output this year.

++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++

This article was updated on November 2, 2023.

The insights presented in this newsletter were made possible thanks to the work of LinkedIn data scientists Yao Huang and Caroline Liongosari.