September 2023 update: Labor markets continue to lose steam, but no signs of an imminent recession yet

Head of Economics and Global Labor Markets at LinkedIn

Subscribe to these updates here.

Global: Overheated job markets in the US and other developed economies are rebalancing without a spike in unemployment

Global: Overheated job markets in the US and other developed economies are rebalancing without a spike in unemployment

There are growing signs that the global economic outlook has witnessed pockets of improvement, driven by steadfast consumer expenditure on services, tempered inflation, and a reduction in immediate risks within the banking sector. Despite much tighter monetary policy than a year ago, the labor market remains resilient in most countries.

Nevertheless challenges persist from increased wages in a competitive job market to rising demand for services, which vary in strength across different regions.

Hiring rates are continuing their year-over-year decline, albeit at a slower pace

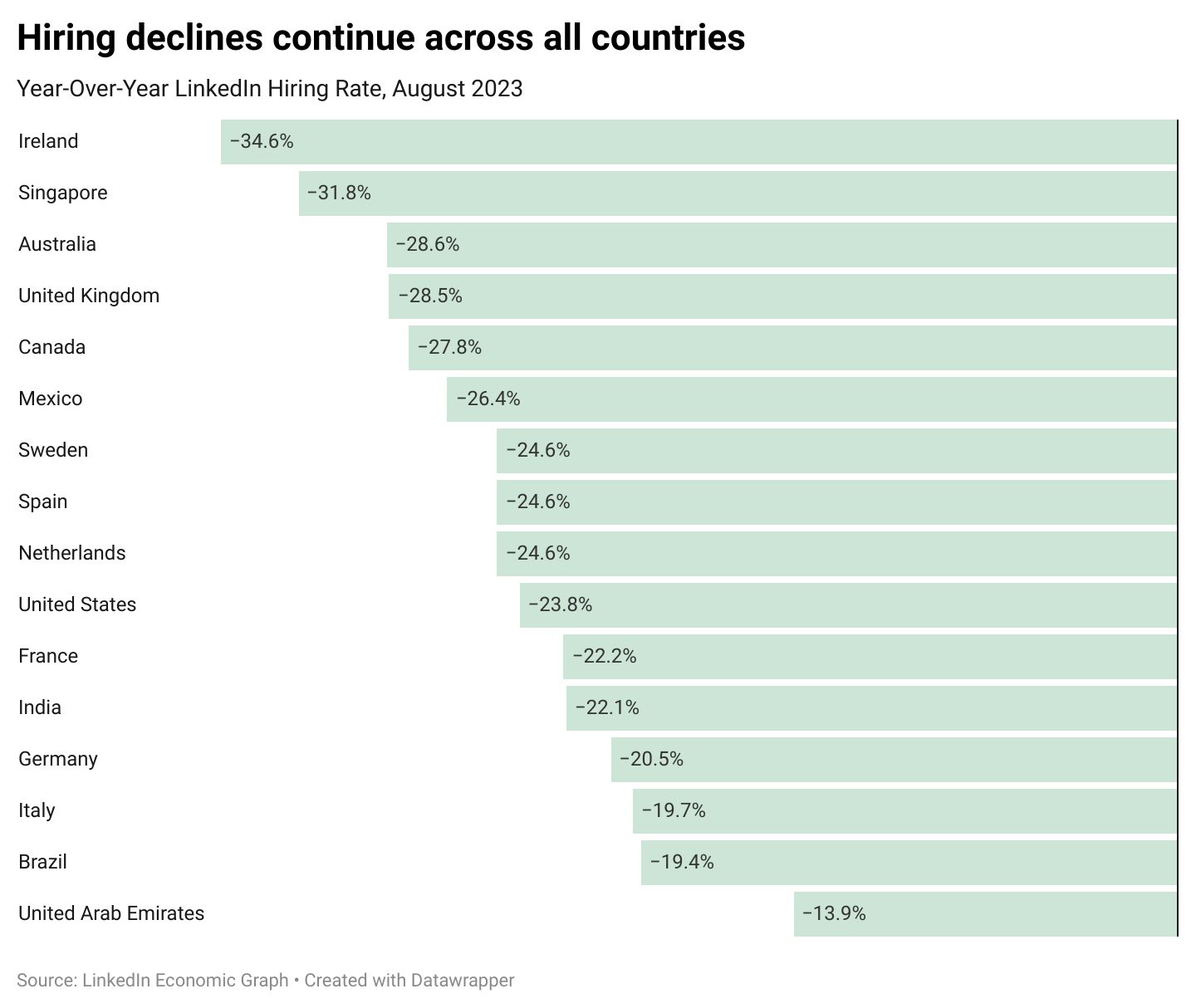

In August 2023, hiring continued its year-over-year decline across most countries. Ireland and Singapore reported the most substantial drops at -34.6% and -31.8%, respectively. Australia (-28.6%), the United Kingdom (-28.5%), and Canada (-27.8%) also experienced significant declines. Year-over-year hiring declines intensified in France (-22.2%) and Germany (-20.5%) compared to the previous two months, whereas India and Italy exhibited a slight slowdown in their decline with -22.1% and -19.7% drops, respectively. In contrast, the United Arab Emirates had a milder decrease of -13.9%.

Applicants are submitting more job applications compared to last year

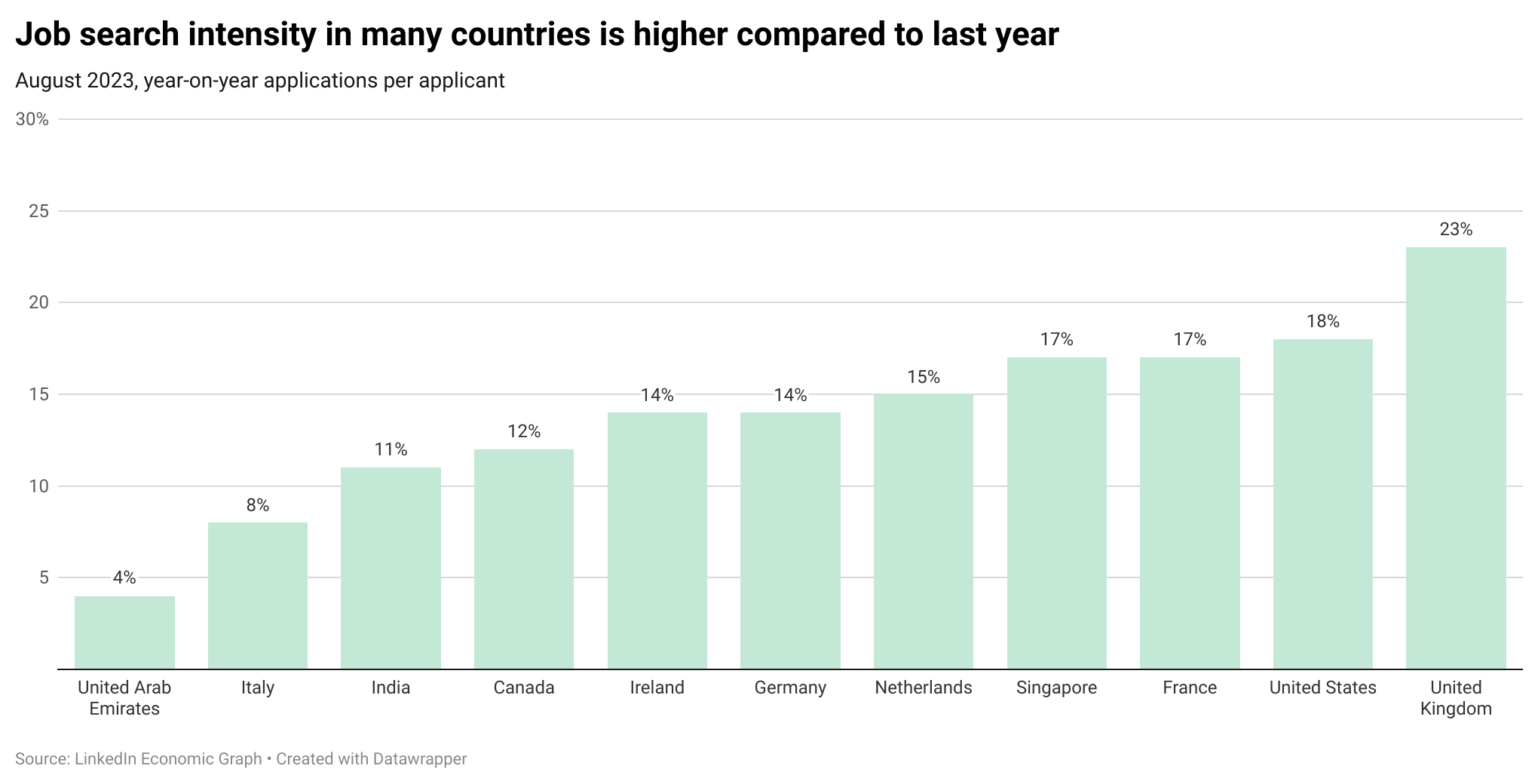

Job search activity has surged in comparison to the previous year, yet there has been a recent deceleration in the rate of growth. In August 2023, the UK witnessed a 23% year-on-year increase in applications per applicant, while the US, France, and Singapore all experienced an increase in search intensity by 18%, 18%, and 17%, respectively. Conversely, the United Arab Emirates observed a more modest year-over-year increase of 4%, likely influenced by the summer and vacation season.

US: The labor market is losing momentum, but the probability of a soft landing is increasing

The US economy has shown robust growth in the first half of the year, thanks to a strong labor market which has enabled consumers to navigate the challenges posed by rising prices and interest rates, reducing the risk of a recession. Nevertheless, when compared to normal times, the medium-term horizon still carries elevated recession risks.

While the likelihood of a recession may be declining, there remain elements that could potentially disrupt the path to economic recovery. These include the possibility of unforeseen inflationary surprises, vulnerabilities stemming from global economic weaknesses, and hidden or unquantified risks lurking within the financial system.

On the employment front, although the labor market continues to exhibit strength, the degree of excess demand is diminishing, primarily due to companies reducing the number of job vacancies rather than resorting to increased layoffs. The decrease in job openings in the US is happening in tandem with a sustained uptick in job seekers’ search activity. Data from LinkedIn indicates that job seekers are conducting more frequent searches compared to the previous year. Specifically, the number of applications per job seeker in the US has surged by 18% year-over-year as of August 2023, suggesting a heightened level of competitiveness in today's job market compared to last year. This increase in search intensity can be partly attributed to reduced confidence among job seekers in their ability to secure employment amidst the prevailing macroeconomic uncertainty.

LinkedIn’s data confirms that confidence among US workers is on the decline

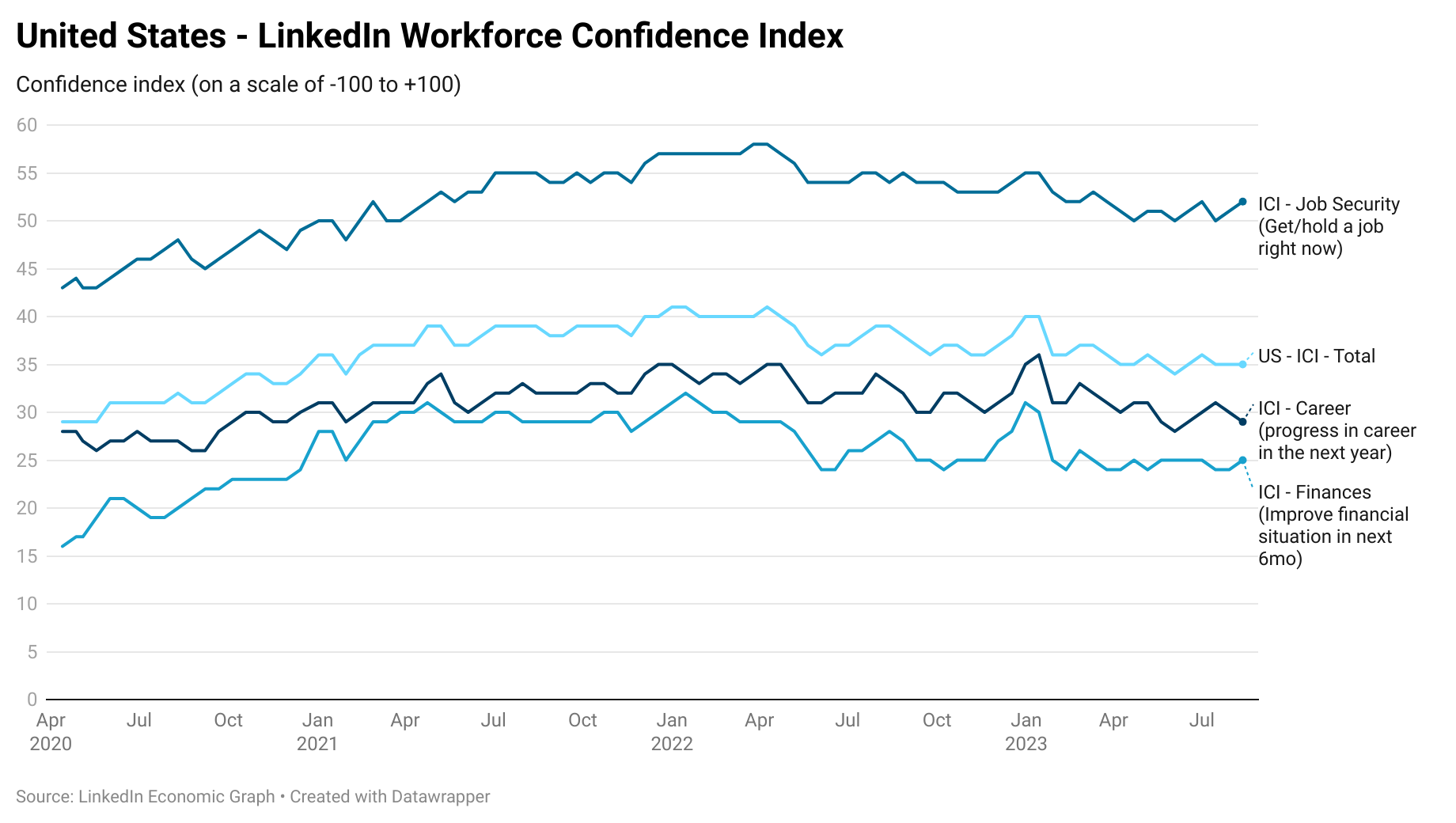

According to LinkedIn’s latest Workforce Confidence Index (WCI), US workers are less confident right now: all confidence indices are lower than the start of the year (January 2023) as well as year-over-year (since August 2022).

Overall WCI currently stands at +35, reflecting a decrease from the beginning of the year (-5 points from +40 in January 2023) and a decline of -3.4 points compared to a year ago (+39 in August 2022).

The Jobs Index, measuring confidence in "getting/holding a job right now," has slightly rebounded to +52 and has remained relatively stable for approximately 5 months. However, it remains lower than the level at the start of the year (-3.6 points from +55 in January 2023) and a year ago (-2.8 points from +54 in August 2022).

The Finances Index, which assesses confidence in "improving financial situations in the next 6 months," is currently at +25, showing a decline of -5 points from January 2023 (+30) and -3 points from August 2022 (+28).

In the Career Index, measuring confidence in "career progression in the next year," the US recorded a score of +29, marking the most significant decline of -7 points compared to January 2023 (+36) and -4 points from August 2022 (+33).

These indices collectively reflect a dynamic landscape of workforce confidence in the US, with notable fluctuations in sentiment across various dimensions of career and financial prospects.

The decline in hiring across almost all industries is another sign that landing a job is becoming more difficult

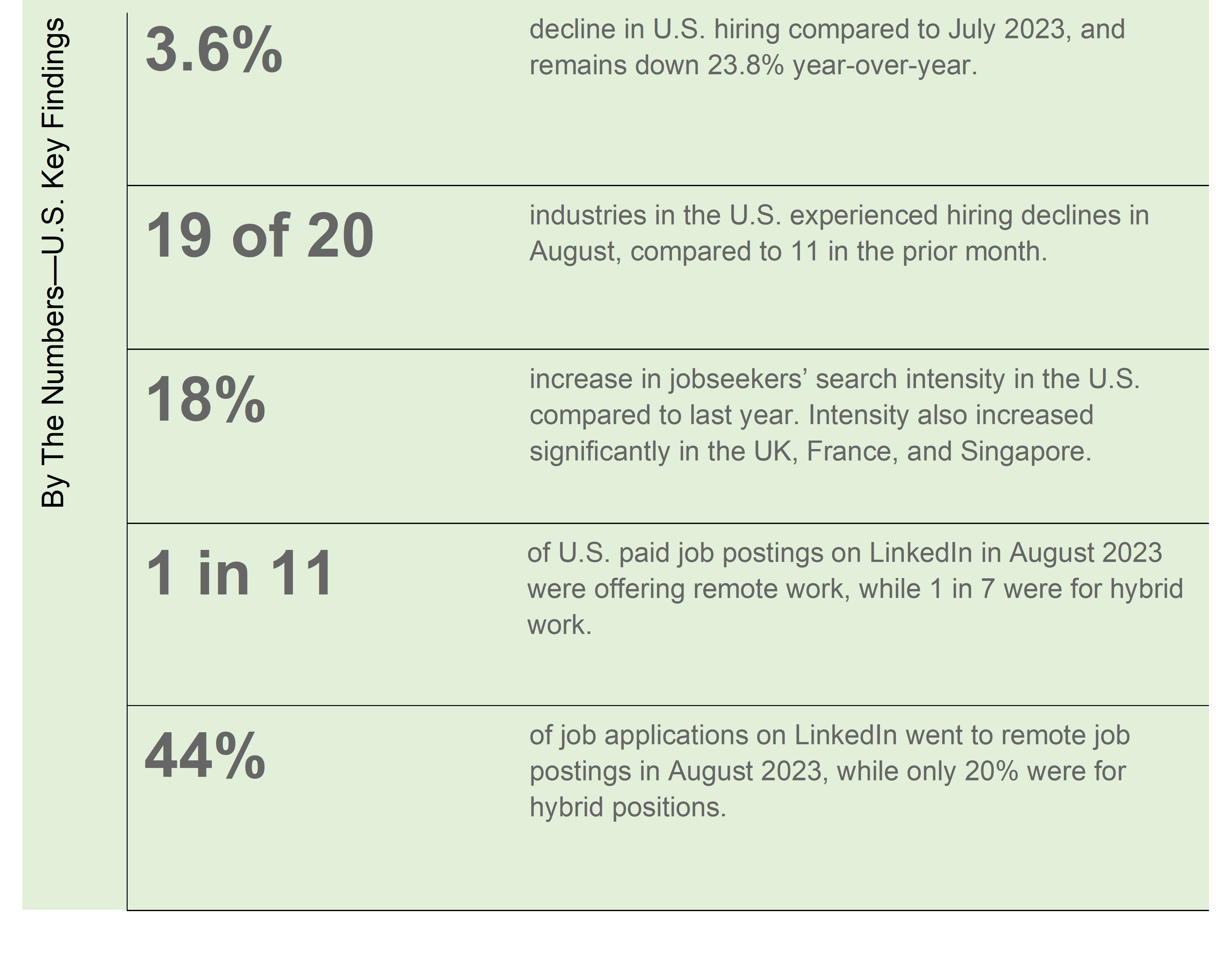

Hiring in the US continued to decline across almost all industries in August 2023, dropping by 3.6% compared to the preceding month, July 2023. This month-to-month decline indicates ongoing turbulence in the employment landscape and reflects the persistent uncertainties that continue to impact hiring decisions among employers.

In August 2023, national hiring experienced a significant decline of 23.8% compared to the same month in 2022. This underscores the ongoing challenges confronting the labor market as it strives to recover the level of strength observed before the disruptions caused by the pandemic.

Individually, various sectors are grappling with their own unique challenges in terms of hiring. The wholesale sector faced a substantial -13.9% month-to-month decline, potentially indicating the ripple effects of supply chain disruptions and trade challenges on employment. Additionally, the retail sector, a vital pillar of the economy, encountered a notable decline with a -10.7% month-to-month change. This could be attributed to factors such as evolving consumer preferences and increased competition from online platforms. Similarly, the accommodation and food services sector recorded a -6.7% decrease in hiring, reflecting the enduring impact of travel restrictions and shifts in consumer behavior.

The financial services industry also experienced a significant setback, with a -7.1% drop in hiring. Complex market dynamics, regulatory changes, and shifts in customer demands likely contributed to this decline.

Remote work is still in play for workers and in our view here to stay

Many professionals are still applying for remote jobs, but employers are increasingly reluctant to offer them. Hybrid however, is on the rise – this aligns with the return to office calls we are seeing.

In August 2023, approximately 9.13% (1 in 11) of US paid job postings on LinkedIn were offering remote work, while 13.9% (1 in 7) were for hybrid work. This marks a decline in remote job offerings from the previous year when they accounted for 17.8% of US paid jobs. In contrast, the percentage of hybrid jobs has been steadily rising since August 2022, when it was 8.8%.

Interestingly, despite the decline in remote job postings over the past year, paid remote jobs continue to attract an outsized share of applications (43.7%) and views (38.8%). Similarly, paid hybrid jobs, with 20.3% views and 20.3% applications, also garner significant attention from job seekers. Overall, 2/3 of job applicants applied to at least one remote or hybrid role last month.

Overall, remote work remains a viable option for employees, and in our perspective, it is likely to persist, albeit at a reduced level compared to the peak during the pandemic.

Employers across various industries are showing an increasing preference for candidates possessing AI-related skills

AI is reshaping the world of work. New LinkedIn data from our Future of Work: AI at Work Report shares never-seen-before insights and trends on how both companies and professionals are adapting. We've observed a growing preference among employers across various industries in the US for candidates with AI-related skills. On our platform, there has been a noticeable increase in discussions and job postings related to AI. However, it's still too early to determine whether AI is significantly impacting job creation or unemployment. Since November 2022, we have seen a substantial 21x increase in the global English-language job postings mentioning GPT or ChatGPT, indicating a growing interest in AI-related technologies. Workers are recognizing the future significance of acquiring AI skills.

In 2022, the 5 fastest-growing AI-related skills, based on year-over-year growth in skills added to member profiles, include: Question Answering: +332% Y/Y, Classification: +43% Y/Y, Recommender Systems: +40% Y/Y, Computer Vision: +32% Y/Y and Natural Language Processing (NLP): +19% year-over-year.

Eurozone: Europe is facing a subdued growth environment

The eurozone is currently grappling with a challenging growth environment with inflation pressuring real incomes, and the region's manufacturing sector is being hampered by weakened external demand. However, a relatively robust labor market, does support the economy.

Several European countries, including Germany, the Netherlands, Spain, France, Sweden, and Ireland, are experiencing significant year-on-year declines in hiring, ranging from 20% to 35%. These declines are attributed to economic uncertainty and labor shortages across various industries. Despite this trend, employment opportunities remain available, with the ratio of job openings to active applicants still higher than pre-pandemic levels in most countries. Additionally, unemployment rates across Europe are historically low or close to them, indicating a relatively robust labor market. This resilience can be attributed to variations in downturns across different sectors and their timings.

United Kingdom: Outlook for economic growth remains muted

Inflation, which appeared to defy gravity earlier this year, has experienced a significant drop in recent weeks, decreasing from 8.7% in May to 6.8% in July. This decline is primarily attributed to base effects as the substantial increases in energy, shipping, and commodity prices from the previous year are no longer impacting the annual comparison. Moreover, the recent inflation decreases have been widespread, and short-term inflation momentum has declined notably, reaching just 1.3% on a monthly annualized basis in June, indicating a reduction in price pressures.

The labor market has remained tight despite the poor economic performance. This is primarily a supply side problem. Employment in the UK has grown by just 0.6% since Q4 2019, compared to a 1.3% growth in the US and 3.1% growth in Europe. Much of the problem is that an extra 520,000 people have left the workforce due to sickness. That’s about 1.5% of total employment that has vanished since the start of the pandemic.

However, there are signs of emerging slack in the labor market. Recent data from August 2023 shows a substantial year-on-year slowdown in hiring, with a significant decline of 28.5%.

Asia Pacific: Labor markets in APAC continue to display resilience despite inflation challenges

Hiring in Australia dropped by -28.6%, while Singapore followed closely behind with a substantial -31.8% decrease. India also faced a notable decline, registering -22.1% less hiring activity year-over-year. These figures collectively highlight the challenging employment landscape in the region, reflecting a substantial decrease in hiring opportunities compared to the previous year.

LatAm: Brazil's economy is wrestling with elevated interest rates and policy uncertainty, while Mexico's economic growth is faltering under the weight of inflationary pressures

In most parts of Latin America, inflation is expected to continue its decline, leading to a broader regional easing cycle in the upcoming months. Brazil's economy is gradually slowing down due to factors such as high interest rates, reduced external demand, and policy uncertainty, which has resulted in a nearly 20% year-over-year decrease in hiring as of August.

Conversely, Mexico's labor market has experienced a substantial 26.4% year-over-year decline in hiring. Mexico's economic prospects are closely linked to the US, and as the USeconomy decelerates, Mexican exports and remittances may be affected. Additionally, elevated inflation and the impacts of monetary policy tightening are dampening domestic consumer demand and business investment. As a result, an easing cycle in Mexico may not commence until the last quarter of 2023 or 2024.

MENA: The MENA region is bracing for a modest downturn in economic activity

The MENA region is gearing up for a moderate decline in economic growth, marking a departure from the decade-long average. This transformation is primarily attributed to a loss of momentum in oil-producing nations, a consequence of the OPEC+ quota reductions. Notably, Gulf economies are poised for a substantial slowdown, while economic growth varies significantly among different countries. In North Africa, the challenges of economic development are compounded by drought conditions, and the region grapples with the adverse effects of rising interest rates and a lethargic global economy.

In the UAE, economic growth is expected to ease in 2023 due to reduced global economic activity, stagnant oil production, and tighter financial conditions. Oil GDP is projected to increase by 2% in 2023, gradually rising to 2.8% and 3% in 2024 and 2025, respectively. The labor market is also cooling, with a 13.9% decline in hiring in August 2023 compared to the previous year. In Saudi Arabia, hiring exhibited a 4.5% year-over-year slowdown in August 2023. Additionally, economic growth in the country is set to decelerate from 8.7% in 2022 to 2.9% in 2023, primarily due to stagnant oil production following OPEC+ quotas.

+++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++

This article was updated on November 2, 2023.

The insights presented in this newsletter were made possible thanks to the work of LinkedIn senior data scientists Yao Huang and Murat Erer.