April 2023 update: Some slack has returned to labor markets, but workers continue to hold power

Head of Economics and Global Labor Markets at LinkedIn

Subscribe to these updates here.

Global: Economic prospects remain relatively subdued

Global: Economic prospects remain relatively subdued

The global economy should weaken this year, before rebounding next year. The impact of last year's monetary policy tightening is expected to continue to weigh on the level of growth for the rest of this year in most advanced economies, while the impact on inflation is likely to be sluggish. The recent bank failures in the U.S. have not affected our baseline predictions for GDP growth. Nevertheless, they do underscore the possibility that a substantial tightening of financial conditions may significantly affect activity. Barring further deterioration in financial conditions, this supports our baseline view of negative growth in major developed economies.

Global output is predicted to decelerate in the remainder of 2023, but recover in 2024. Our baseline forecast remains a mild recession in the U.S. and the UK, very modest but positive growth in continental Europe and LatAm, and solid growth in the APAC and the MENA regions.

We expect inflation to fall back for most economies due to lower commodity prices, decelerating growth, and mitigated supply chain problems. Nevertheless, the speed and scale of this decline will differ from one economy to another, depending on the relative importance of supply and demand factors in pushing up inflation in 2021 and 2022.

Although hiring across the globe has continued to slow down in recent months, job markets remain resilient. The ratio of job openings to applicants is still above the pre-pandemic baseline in multiple countries, and unemployment rates are hovering near historical lows.

Uncertainty surrounding the economic outlook has caused companies worldwide to scale back their hiring plans. At the same time, labor shortages in many countries have resulted in employers competing for a smaller pool of workers, putting upward pressure on wages and exacerbating the tightness of the labor market. Although LinkedIn’s measure of labor market tightness, which compares job openings to active applicants, is gradually approaching its pre-pandemic average in countries such as the U.S., UK, Canada, India, Ireland, and Singapore, it still remains tighter than its pre-pandemic baseline in several European countries, including Germany, France, Italy, and the Netherlands.

As labor markets cool down, job seekers are intensifying their search efforts, realizing that they may no longer have the luxury of taking their time. In many countries, the average number of applications per applicant has substantially increased compared to the same month last year. In March 2023, the average number of applications per applicant in the U.S. increased 35% year-on-year, while in the UK, it increased by 36%. In Ireland and the Netherlands, it increased by 31%. In France and Italy, the increase was smaller, at 12% and 7% year-on-year, respectively.

U.S.: Some slack is returning to the labor market

Recent data indicates that employers are opting for caution, as hiring in the U.S. declined by 28.2% in March 2023 compared to the same period in 2022. The decline was noted across all industries, with the technology, information, and media sector experiencing the largest year-over-year hiring shift at -50.1%, followed by holding companies at -34.3%, professional services at -31.8%, and financial services at -30.2%.

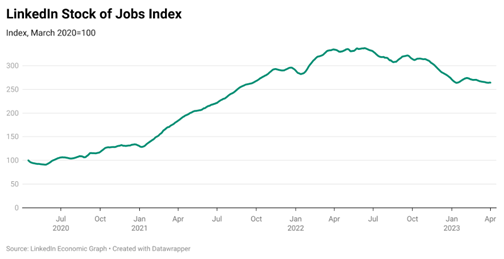

Although hiring slowdowns don’t necessarily indicate an impending recession, they are coinciding with other indicators that suggest a return of some slack to the labor market. Job openings have been slowing down and the ratio of openings to active applicants on LinkedIn has also decreased from the peak observed in mid-2022 when it was predominantly a job seeker’s market. Throughout most of 2022, there was nearly one job opening for every job seeker on LinkedIn, which meant that professionals largely had the edge in commanding higher salaries, better titles, and more flexibility.

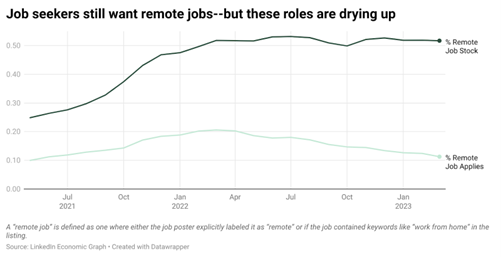

Despite the recent cooling in the labor market and slowdown in hiring, job openings on LinkedIn remain higher than pre-pandemic levels. Although there has been a gradual deceleration in the number of overall jobs and the underlying share of remote jobs, which dropped to 11.8% (1 in 9) of total job postings from the peak of 20.6% in March 2022, there are still opportunities available for those seeking work. While hiring has declined notably, it is important to note that it has slowed from historic highs during 2021. As a result, workers still have some bargaining power gained and it is still a job seeker’s market in some sectors.

Despite a cooling labor market, some industries are still struggling with filling jobs

The deceleration in hiring is consistent with the general trend of cooling labor markets, as evidenced by the decrease in the job openings to active applicants ratio since the summer of 2022. Nevertheless, this trend is not uniform across all industries. Labor market conditions in accommodation, oil and gas, manufacturing, and hospitals and healthcare are still very tight in comparison to the pre-pandemic era. In these sectors, employers are struggling to find qualified candidates to fill available positions, resulting in a competitive hiring environment where the job openings to active applicants ratio exceeds pre-pandemic levels. The steady demand for workers in accommodation shows the underlying strength in a sector that is defined by people going out and spending on things like vacations, hotel stays, and restaurants.

On the other hand, job seekers in industries such as government administration, consumer services, education, technology, information and media, professional services, finance, transportation, and entertainment are often applying for multiple jobs before they secure a job. As a result, employers in these industries have been able to fill vacancies without increasing wages. These sectors are currently experiencing a slowdown, with the ratio of job openings to active applicants dropping below pre-pandemic levels.

Despite tight conditions in some industries, the appeal of remote work remains elevated, even as postings for remote jobs decline. Although there are fewer remote work postings than in-person postings, the former continue to receive over half of the total applications (51.6%).

Moving forward, the continuous strength in the labor market and the pace of job growth is likely to leave the Fed on track for further tightening at the next meeting, pushing the Fed funds rate up closer to the 5%-5.25% range.

Eurozone: Job markets across Europe remain very tight

The Eurozone economy is weathering a period of turmoil, following the collapse of several U.S. banks and the resolution of the Credit Suisse crisis with its absorption by rival bank UBS. Despite the limited risk of systemic contagion, there are growing concerns about the financial system’s health and the effects of surging interest rates. Although no economic data is currently available to measure the turmoil’s impact on the actual economy, we will need to wait to assess its complete influence on activity. Nonetheless, the tightening in financial conditions that has taken place will undoubtedly affect growth over the upcoming quarters. Despite activity faring better than expected and inflation having peaked in Q4 2022, the Eurozone economy continues to be weak, with an uncertain outlook. In general, our assessment indicates that there will be no significant expansion in the economic growth of the Eurozone during the first quarter of this year.

Furthermore, in addition to the uncertainty regarding energy prices and the war in Ukraine, the complete impact of the current monetary tightening remains unclear, given the ECB is still raising rates at a significant pace. Almost all European countries are experiencing a significant slowdown in hiring year-on-year, including Germany (-22% YoY), the Netherlands (-27% YoY), Spain (34% YoY), France (-32% YoY), Italy (-30% YoY), and Ireland (40% YoY). Economic uncertainty has played a significant role in this trend, leading to a decline in business activity and a decrease in demand for talent across various industries.

Notwithstanding the sluggish economic conditions, LinkedIn’s data still point to labor market resilience. In most countries, the ratio of job openings to active applicants remains higher than pre-pandemic levels, and unemployment rates are either at or close to historically low levels, both nationally and across the entire region. The continued resilience, combined with persistently high core inflation figures, is likely to reinforce the ECB’s hawkish stance on further policy tightening.

UK: Britain’s labor market is showing further signs of cooling

Due to lower wholesale gas prices, the UK is likely to experience a milder recession than previously forecasted. The bigger picture in the UK reveals an economy that is likely to experience a shallow recession in 2023 due to tight policy settings and falling real household income. Inflation is predicted to have already reached its peak, but it is expected to persist at a high level throughout 2023.

The latest data suggests that the job market, which was once thriving, is now displaying signs of a slowdown. While job openings remained high in Q4 2022, hiring has been on a steady decline since last summer, indicating a reduced demand for UK workers. Data from March 2023 shows a significant year-on-year decrease in hiring activity, with a sharp 34% decline compared to the same period last year. However, the strong labor market should limit how far unemployment rises in any upcoming slowdown.

The job openings to active applicants ratio has reverted to its pre-pandemic level. Looking ahead, labor market conditions are expected to continue to cool, but the unemployment rate is predicted to stay lower than in previous economic downturns.

Asia Pacific: Hiring in APAC has significantly slowed down on a year-on-year basis

Most of the region’s economies will experience a marked slowdown in 2023. Indeed, in many, a sharp deterioration was already evident at the end of 2022. Our data conveys a similar message: the labor market is showing some indications of loosening conditions. LinkedIn’s measure of labor market tightness, the job openings to active applicants ratio, is moderating toward pre-pandemic levels in the APAC region. In Australia, there are approximately three active job seekers competing for each job opening, while in Singapore, the labor market is showing slightly more slack, with five active applicants per job. India has considerably more slack, with 17 active applicants competing for each job opening. However, based on government statistics, unemployment rates are currently at the lowest level in 50 years, suggesting that individuals who are still employed are searching for alternative employment opportunities.

Amid the cooling labor market, hiring continues to level off after reaching historic highs in early 2022. Singapore and India have both experienced a substantial year-on-year slowdown in hiring, with declines of 43% and 40%, respectively, in March 2023. This trend can be attributed to a variety of factors, including increased economic uncertainty and shifting market conditions. Australia has seen a slightly lower decline, with hiring slowing down by 35% year-on-year.

Latin America: Labor markets are slowing as hiring falls across the region

Latin America's economic prospects are looking difficult, as five of the six largest economies in the region – namely Argentina, Brazil, Chile, Colombia, and Mexico – are projected to experience a synchronized, though mild, recession in 2023 according to Oxford Economics. On average, LatAm GDP indicates that it will remain largely stagnant in the coming year, as a result of a triple threat to the region's economic growth, caused by weaker global demand.

According to the latest hiring data, Brazil and Mexico have experienced significant year-on-year slowdowns in hiring. In March, Brazil saw a decline of 28%, while Mexico experienced an even more substantial decrease of 37%.

Gulf Cooperation Council: The labor market outlook for the GCC region appears more upbeat in comparison to the rest of the world

Although the GCC region's outlook is favorable compared to global trends, the pace of its GDP growth is predicted to decrease by more than half to 2.5% this year, from 5.1% in the previous year. The deceleration is expected to intensify due to oil production cuts and stricter policies. The near-term forecast will continue to be limited by high inflation and elevated borrowing costs, which will dampen demand and economic activity.

Despite weaker oil prices and reduced production, the UAE's oil sector revenues are projected to remain strong, enabling the government to sustain overall GDP growth this year. However, the Saudi Arabian economy is anticipated to slow down from last year's robust growth rates due to a weaker global environment and stagnant oil production. Hiring in the UAE dropped by 26% year-over-year, while in Saudi Arabia, it dropped by 19%. This trend may be attributed to various factors such as changing market conditions and increased uncertainty in the outlook.

In Focus: Displacement of technology, media, and information workers

U.S. workers displaced from the technology, media, and information industry, as measured by members with the Open-to-Work (OTW) feature turned on between the old position start date and the new position start date, are increasingly transitioning to other industries, with the exodus rate increasing from 57% in April 2022 to 65% in Feb 2023.

In 2023, the top industries, excluding the technology, information, and media industry itself, where displaced workers transitioned to, were Professional Services (20.4%), Financial Services (8.1%), Manufacturing (7.7%), Administrative and Support Services (4.0%), Hospitals and Healthcare (3.5%), and Entertainment Providers (3.2%). These are the top industries workers from the technology, information, and media industry have transitioned to the most over the past two years – and this trend is also observed in other regions outside the U.S. as well.

Other U.S. industries that have been increasingly attracting tech talent between 2021 and 2023 are accommodation (+50% Yo2Y), administrative and support services (+38% Yo2Y), consumer services (+35% Yo2Y), hospitals and healthcare (+16% Yo2Y), and transportation, logistics, supply chain and storage (+10% Yo2Y). While the absolute share of transitions into these industries is relatively small, they have consistently grown over the past two years as destination industries for workers displaced out of the technology, information, and media industry. It's worth noting that similar trends have also been observed in other countries, where tech workers are increasingly seeking employment opportunities in alternative industries.

Finally, LinkedIn data on technology, information, and media transitions suggest that big companies’ talent loss is small companies’ gain. In the U.S., workers from large companies (10k+) appear to be increasingly transitioning to smaller tech firms with the share having increased from 52% to 72% from Jul 2022 to Feb 2023.

++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++

This article was updated on November 2, 2023.

The insights presented in this newsletter were made possible thanks to the work of Pingyu He, Yao Huang, Murat Erer, and Danielle Kavanagh-Smith, all of whom are members of LinkedIn’s Economic Graph team.