June 2023 update: Workers’ grip is slipping, despite job market’s resilience

Head of Economics and Global Labor Markets at LinkedIn

Subscribe to these updates here.

Global: Tight monetary policy to weigh on business and household activity

Global: Tight monetary policy to weigh on business and household activity

The global economy kicked off 2023 with strong momentum, registering growth of approximately 0.7% (non-annualized) in the first quarter compared to the previous quarter. Despite tighter monetary policy across numerous economies, labor markets reamained resilient. However, the factors indicating a potential slowdown in growth still hold true. The initial boost experienced by the Chinese economy following the lifting of zero-Covid restrictions seems to be losing steam, and the consequences of previous monetary policy tightening in advanced economies are continuing to accumulate. Looking ahead, we anticipate a slowdown in industrial momentum throughout 2023 and a gradual deceleration in global GDP growth throughout the remaining months of this year.

Hiring is down across the globe and employers are slowly regaining the upper hand

The uncertain economic outlook has prompted companies worldwide to reduce their hiring plans, although the year-on-year hiring declines appear to be moderating in a few countries. Concurrently, labor shortages in many countries have intensified the competition for a limited pool of workers, exacerbating labor market tightness.

While countries like the U.S., UK, Canada, India, Ireland, and Singapore show more signs of slack as LinkedIn's measure of labor market tightness gradually approaches pre-pandemic levels, several European nations, including Germany, France, Italy, and the Netherlands, continue to face tighter conditions compared to their pre-pandemic baseline. This cooling trend suggests a potential shift in the balance of power, indicating that workers are experiencing reduced influence in the job market. Consequently, this development may contribute to a slowdown in wage pressure and inflationary pressures.

Furthermore, the increased uncertainty in the outlook has triggered a substantial rise in the level of job seekers' search activity. Individuals are actively pursuing more secure employment opportunities, and those who had previously remained on the sidelines are now reentering the labor market. Notably, in the United States, the number of job applications per applicant on LinkedIn has observed a significant year-on-year increase of 35%. Similarly, the United Kingdom has witnessed a 38% surge in job search intensity, followed by Ireland at 33% and Canada at 31%. Comparatively, Italy and India experienced a more modest increase at 13%.United Arab Emirates displayed a noteworthy rise in search intensity this month, reaching 17% year-on-year, surpassing levels seen in previous months.

US: Despite some gradual cooling, abundant bright spots continue to shine through

The current stress in the banking system has resulted in tighter lending conditions, narrowing the path to a soft landing for the US economy compared to a few months ago. The strength of consumption plays a crucial role in determining the outcome. Over the past six months, the consumer sector has been instrumental in sustaining the economy, and it is likely to continue being a significant source of strength for the remainder of the year. Our baseline forecast predicts a mild “rolling recession” towards the end of CY 2023, with economic activity declining in some industries more than others. Rather than an abrupt contraction in economic activity across all sectors of the economy, we are likely to see various sectors of the economy take turns contracting rather than simultaneously.

The downward trend in hiring that we witnessed over the past several months has begun to stabilize

In May 2023, hiring in the United States across all industries demonstrated signs of leveling off, with a modest increase of 3.5% compared to the previous month of April 2023. However, when compared to May 2022, hiring on LinkedIn is down by 21.8%. These statistics indicate a leveling out in the hiring landscape, suggesting that the rapid cuts witnessed in previous months has tapered off a bit. It’s still too early to tell whether the hiring increases will continue or the previous declines will resume. The slowdown in hiring varies across industries, with the technology, information, and media sector experiencing the most pronounced deceleration year-over-year.

Even during this continued uncertainty, it’s still a good time to be entering the economy as an entry-level job seeker

Although hiring for entry-level positions in the US has also dropped, there’s still a lot of demand for people in a handful of industries, especially for roles requiring in-person attendance. For career starters currently looking for their first (or next) role, the job market remains relatively robust, albeit with a heightened level of uncertainty compared to the previous year. According to a survey from the National Association of Colleges and Employers, employers are planning to hire almost 15% more graduates from the Class of 2023 than they did in 2022. Although this would be a substantial increase in hiring, it is less than half of the final increase employers had projected for the Class of 2022 (31.6%).

Entry level opportunities abound in healthcare, professional services, and manufacturing

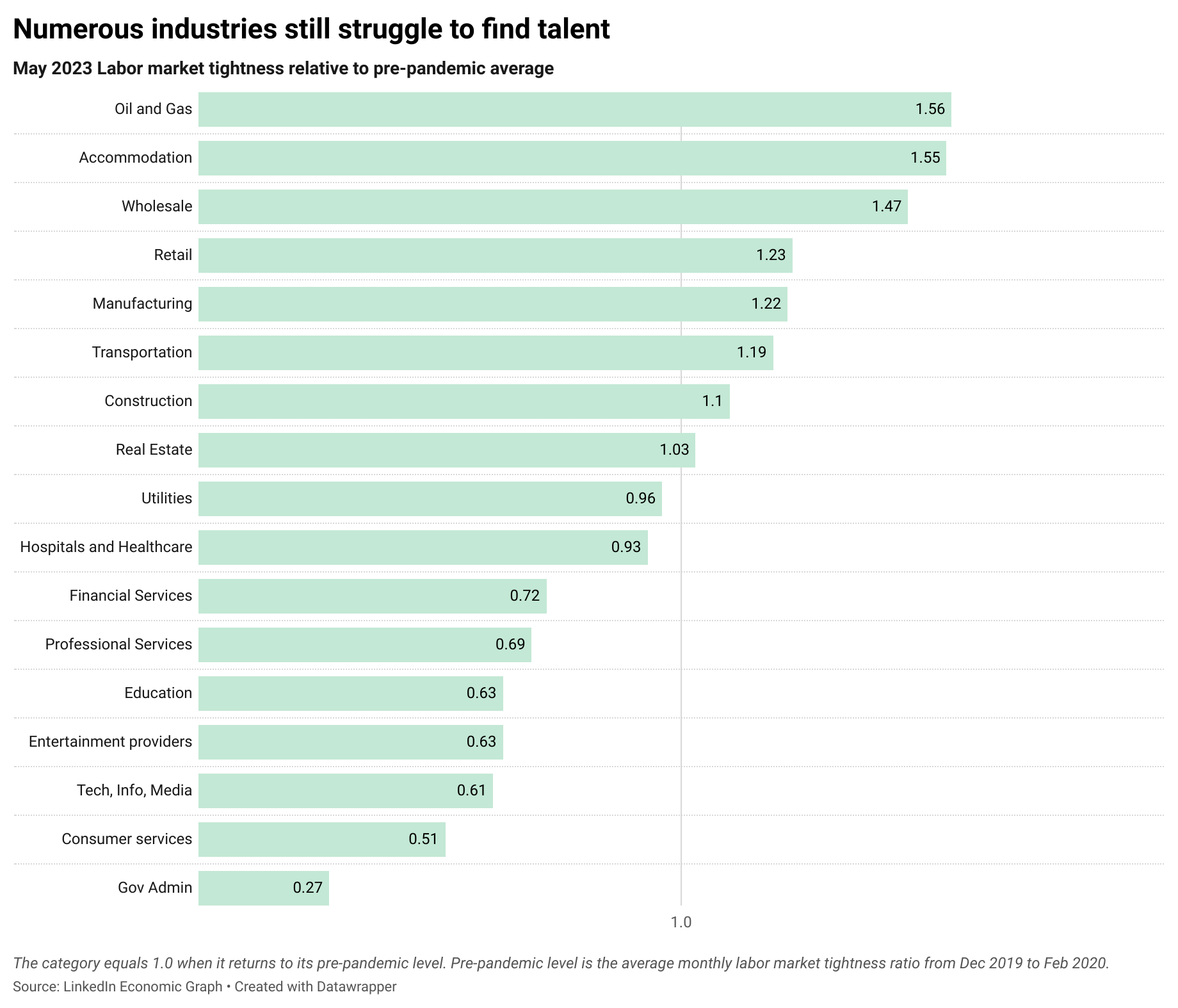

Zooming into specific industries, according to our recently released Guide to Kickstarting Your Career, healthcare, professional services, and manufacturing are the sectors that saw the biggest gains in entry level job opportunities for career starters in the last year. In these sectors, positions such as medical assistant, paralegal, and maintenance technician ranked among the top jobs for individuals without a four-year degree. These sectors are also among the industries that have tightened much over the past two years, and continue to be tighter than their pre-pandemic averages. In other words, there’s still a significant gap between the number of available jobs and the supply of workers compared to where we were before the pandemic.

Focusing on industries with the highest hiring rates is just as valuable as paying attention to roles that are experiencing rapid growth in hiring. According to LinkedIn data, the professional services industry, which encompasses fields such as accounting and management consulting, stood out as a leader in this regard by hiring the largest number of bachelor's graduates in 2022.

Some states are still hungry for talent, making them hotspots for career starters

While the national labor market shows signs of cooling, a deeper dive into state-level dynamics reveals an intriguing story. We turn to LinkedIn's job openings-to-applicants ratio to uncover the variations in recovery across different geographical regions, especially when compared to pre-pandemic conditions.

In an encouraging trend, 39 states outshine their pre-pandemic labor market conditions, offering a plethora of opportunities for job seekers, particularly career starters and younger adults. These states present an attractive landscape, with an abundance of jobs awaiting eager professionals. Remarkably, in 8 of these states, labor market tightness exceeds pre-pandemic levels by more than 50 percent. Leading the charge are Maine (+128 percent), Alaska (+61 percent), Kentucky (+55 percent), South Dakota (+54 percent), and Wisconsin (+53 percent) experiencing remarkable surges in available positions.

Conversely, labor markets in 12 states (including D.C.) exhibit less tightness compared to their pre-pandemic state. However, it's important to note that the gap in these states remains relatively small. Job seekers in these regions face heightened competition as the abundance of job seekers vies for the available positions.

For career starters and younger adults seeking an advantageous entry into the workforce, these states with thriving labor markets offer a promising arena to kick-start their professional journey. Keep a close eye on these hotspots, where opportunity abounds and the potential for growth is tangible. For more cities that have been fast growing amongst career starters, our full report is here.

Employees remain drawn to remote work, but younger adults interest in remote work lags behind other generations

In May 2023, LinkedIn data showed that paid remote jobs on LinkedIn attracted 47% of applications, compared to 19% for hybrid. Interestingly, when we looked at which generations are applying to remote jobs, Gen Z lags behind Millennials and Boomers. They are the least likely among all workforce generations to apply for remote work, and are more likely to apply for hybrid roles. Gen Z’s interest in remote work has been slowing: 37.5% of Gen Z’s job applications in May 2023 are to remote roles in the U.S., down from 45% in May 2022. There’s a sense that this generation is still looking to retain certain elements of in-person connection and collaboration, given many entered the job market amidst the global pandemic and have yet to experience office life and on-site work.

Where can people find remote and hybrid jobs?

Since the desire for remote work is still strong and the number of companies offering fully-remote work is decreasing, we continue to be in a situation where demand outweighs supply. Linkedin data show Professional Services (22.6%), Technology, Information, and Media (20.4%), and Administrative and Support Services (16.0%) are the industries with the greatest percentage of remote job postings in May 2023. Industries for the greatest percentage of hybrid paid job postings are Professional Services (30.4%), Utilities (24.1%), and Financial Services (23.0%).

Securing a fully remote job has become more challenging compared to hybrid or onsite roles. As a result, job seekers entering the labor market today, especially career starters, may have a higher chance of landing a job that doesn't require them to work fully from home.

Which job functions are attracting new grads in today’s climate?

In light of employers' growing emphasis on skills, recent data from LinkedIn also sheds light on the job functions that are expanding most rapidly for bachelor's degree holders entering the workforce. At the top of the list is product management, witnessing a remarkable 26% increase in hiring between 2021 and 2022. In addition, consulting (+17%), purchasing (+13%), human resources (+13%), and business development (+11%) are identified as the five fastest-growing functions for recent graduates during that period. It is worth noting that consulting and human resources also feature prominently among the rapidly growing job areas for career starters without a bachelor's degree.

Eurozone: Tight Labor market conditions persist in Europe

While our baseline forecast suggests that the eurozone economy will manage to steer clear of a recession, the growth prospects for this year and the next remain fragile. We anticipate that factors such as persistent inflation, elevated interest rates, tighter financial conditions, and deteriorating external environment will contribute to sluggish economic progress in the eurozone. However, even in the face of lackluster growth, the labor market within the eurozone continues to showcase remarkable resilience.

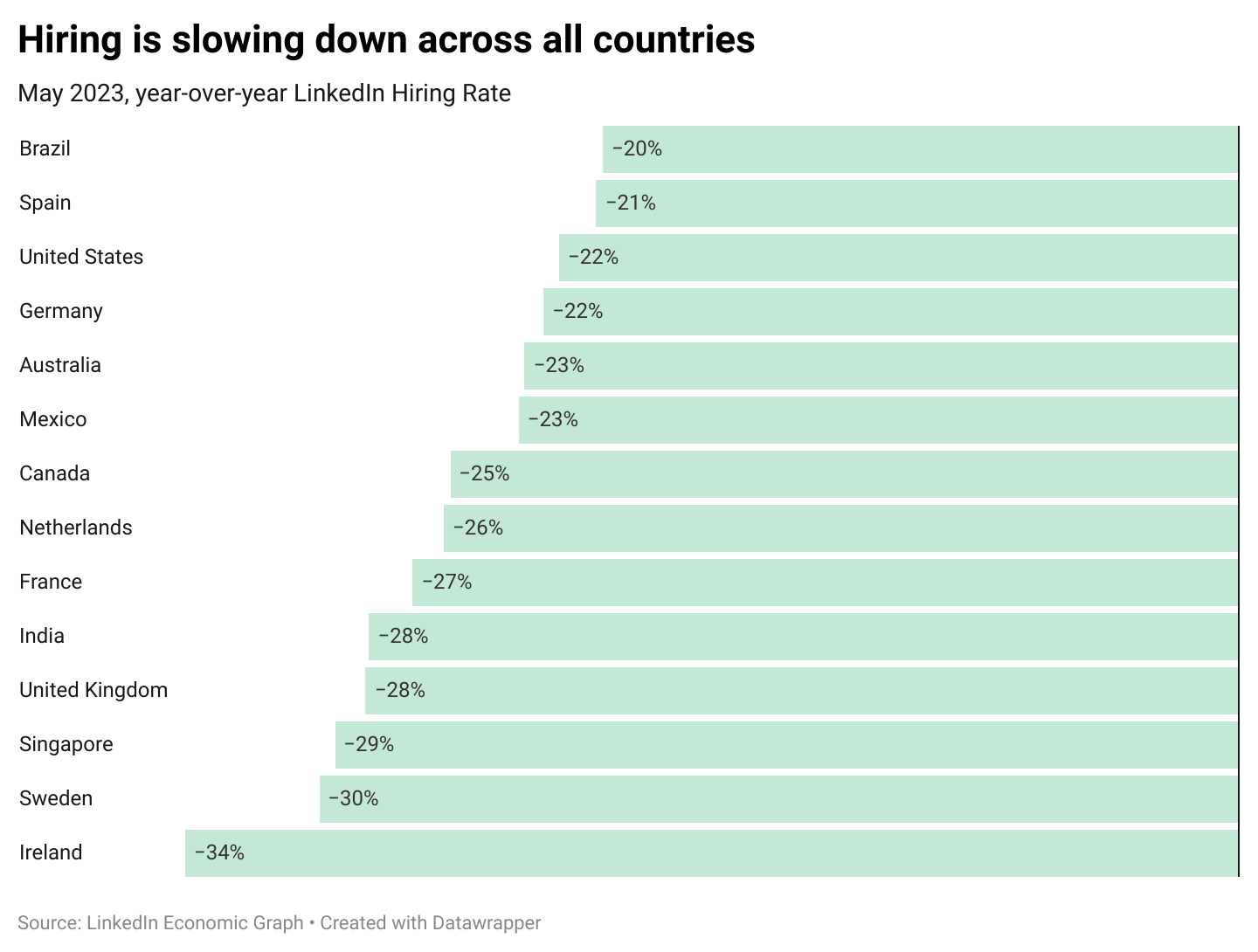

Almost all European countries are experiencing a significant decline in year-on-year hiring, including Germany (-22% YoY), the Netherlands (-26% YoY), Spain (-21% YoY), France (-27% YoY), Sweden (-30% YoY), and Ireland (-34% YoY) being among them. While economic uncertainty remains a significant contributing factor, labor shortages in various industries are also playing a crucial role in this trend. However, despite the slowdown in hiring, there are still employment opportunities for individuals seeking work. In most countries, the ratio of job openings to active applicants remains higher than pre-pandemic levels, and unemployment rates either stand at historically low levels or hover near them, both nationally and across the entire European bloc. The robustness of the labor market can be attributed to a combination of factors, including the variations in downturns across different sectors, occurring at different times.

An alternative and compelling explanation for the remarkably robust labor market could be attributed to firms retaining their workforce (labor hoarding). As concerns of a severe and prolonged downturn fade away, businesses may be hesitant to downsize their workforce, even during periods of weak demand, with the expectation of rehiring employees once activity rebounds in the future. This hoarding behavior is further intensified by the already limited availability of jobseekers in a tight labor market, making it even more challenging for firms to compete for talent. In a way, this dynamic creates a self-fulfilling prophecy, where firms' expectations of a moderate downturn and a tight labor market contribute to the ongoing tightness in the labor market itself.

United Kingdom: The UK labor market is showing signs of easing, with decreased demand for workers

Ongoing industrial disputes are expected to weigh on GDP in the second quarter. Despite strong early business survey data, a small decline in Q2 GDP is still anticipated. However, the recovery is projected to gain traction in the second half of 2023 as the impact of strikes diminishes and falling energy prices lead to a recovery in real incomes. With favorable historical data revisions, the GDP growth forecast for this year has been revised up to 0.4% from 0.3% last month. The forecast for 2024 GDP growth remains unchanged at 1.3%. However, the recovery may face challenges due to tighter financial and credit conditions resulting from recent banking system strains, as well as the impact of tight monetary and fiscal policies.

Several indicators pointed to evidence of looser labor market conditions in Q1. In particular, the unemployment rate increased to 3.9%, marking the highest quarterly rate since the fourth quarter of 2021. This rise was primarily driven by a surge in labor supply as more individuals entered the job market in search of employment. Concurrently, the number of job openings on LinkedIn continued to decline, leading to a continuous gradual decline in the ratio of job openings to active applicants, LinkedIn measure of labor market tightness.

Along with a notable return of slack to the UK labor market, a sustained downward trend in hiring has been observed since the previous summer, signaling a decreased demand for workers in the UK. The latest data from February 2023 highlights a significant year-on-year decrease in hiring activity, with a sharp decline of 28 percent compared to the corresponding period in the previous year.

The bigger picture for the UK labor market remains promising. The tightening of labor market conditions observed over the past few years was largely influenced by a decline in labor supply. A significant factor contributing to this decline was the decrease in labor force participation, which can be attributed to both the aging population and increased rates of inactivity among individuals of working age. The latest data suggests that the post-pandemic fall in participation is reversing rapidly.

Asia Pacific: Hiring momentum in the APAC region has started to level off, with signs of slack appearing in the labor market

In Q1, growth data in Asia varied across the region, with some countries being boosted from China’s reopening - for example the tourism sector across countries in South-East Asia helped to buoy economic growth, while increased energy exports to China also supported growth. In other countries, there was more moderate growth due to global slowing, such as Singapore which faced a slowdown as the technology sector slowed and electronics exports declined.

These divergent outcomes can be attributed to factors such as reopening effects, the technology downturn, and exchange rate differences. While these factors are expected to be temporary, cautious GDP forecasts for the rest of the year anticipate that the negative effects will persist longer than the positive ones.

Our data indicates that hiring, which reached historic highs in early 2022, has started to level off. Singapore and India have both encountered a significant year-on-year decline in hiring, with drops of 29% and 28%, respectively, in May 2023. This trend can be attributed to various factors, including heightened economic uncertainty and shifting market conditions. Australia has witnessed a slightly lesser decline, with hiring slowing down by 23% year-on-year.

The ratio of job openings to active applicants, a metric used by LinkedIn to measure labor market tightness, is cooling back to pre-pandemic levels. Both Australia and Singapore exhibit similar levels of tightness, with 4 and 5 active applicants per job opening, respectively. India, on the other hand, displays a slightly higher competition for jobs, with 17 active applicants per job opening. However, it's important to note that based on government statistics, unemployment rates in the region are currently at their lowest levels in 50 years.

LatAm: Latin America faces economic slowdown despite slight improvement

Latin America's largest economies, including Argentina, Brazil, Chile, Colombia, Mexico, and Peru, have seen mixed growth trends in the first quarter. While our regional aggregate GDP growth estimate has improved to 0.1% quarter-on-quarter from a contraction previously, individual countries exhibit divergent patterns. Peru and Argentina likely experienced contraction, while Chile and Colombia have higher-than-expected growth risks.

Brazil's GDP outlook is uncertain due to publication delays, but we anticipate positive quarterly growth. Mexico's preliminary GDP data showed a 1.1% expansion, surpassing expectations, yet we still anticipate a mild recession in the second half of the year. Hiring slowed down by 21% year-over-year in Brazil and by 23% in Mexico.

Gulf Cooperation Council: Labor market outlook for the GCC region remains positive despite slowdown in growth

Data from the GCC region points to continued resilience of the regional economy. Strong domestic demand has helped offset global headwinds, driving economic activity. Central banks in the GCC raised their policy rates by 25bps, following the US Fed, marking the likely end of the tightening cycle. Elevated interest rates are expected to dampen non-oil sector growth in the GCC to 3.9% in 2023. Most recent data indicates that domestic demand remains a key growth driver in the GCC, while export orders face challenges from global headwinds. Inflationary pressures are easing, supporting private consumption and overall activity, although UAE companies have faced greater input cost pressures compared to their Saudi and Qatari counterparts.

In the UAE, although the ratio of job openings to active applicants experienced a year-on-year decline of -25% in May 2023, the labor market demonstrated its resilience with a mere 4% decrease in hiring compared to the same period last year. While inflation rates in the UAE and other countries in the GCC region are generally decreasing, influenced by a decline in global commodity prices, there are also various country-specific factors contributing to these trends.

+++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++

This article was updated on November 2, 2023.

The insights presented in this newsletter were made possible thanks to the work of LinkedIn data scientists Yao Huang and Caroline Liongosari.